Written by the InclusivePay Merchant Advisory Team | Last updated: April 2026

InclusivePay has been placing CBD merchants since 2018. This guide covers what actually gets CBD oil merchant accounts approved — and the silent mistakes that get them shut down.

If you sell CBD oil — tinctures, capsules, softgels, gummies, edibles — you already know payment processing is harder than it is for topicals. Banks and underwriters treat ingestibles differently. The regulatory exposure is higher, the chargeback potential is higher, and the list of processors willing to touch it is shorter.

That doesn’t mean it’s impossible. InclusivePay has been placing CBD oil merchants since 2018 and we do it constantly. But there are specific things that get CBD oil accounts approved — and specific things that get them shut down — that most guides completely miss. This is what you actually need to know.

Why CBD Oil Is Harder to Process Than Topicals

Not all CBD is treated equally by acquiring banks. Topicals — balms, salves, creams applied to the skin — sit at the lower end of the CBD risk spectrum. Ingestibles — oils, tinctures, capsules, gummies, beverages — sit higher. Here’s why.

- Higher chargeback potential Customers who consume CBD oil and don’t experience the effect they expected dispute the charge. “Didn’t work” is a subjective claim that’s hard to fight in a chargeback dispute. Topicals have a lower dispute rate.

- FDA scrutiny on ingestibles The FDA has not approved CBD as a food additive or dietary supplement. Ingestibles marketed with any health benefit language draw more regulatory attention than topicals.

- Higher health claim risk The temptation to make efficacy claims is greater with ingestibles. “Helps with sleep,” “reduces anxiety,” “supports pain relief” — any of this language on your site or packaging can terminate your account regardless of how compliant your COAs are.

- State-level restrictions Some states have specific restrictions on CBD edibles and ingestibles that don’t apply to topicals. Your processor needs to understand the states where you’re selling.

None of this means you can’t get a merchant account. It means you need a processor with actual experience placing CBD oil merchants — not one that placed a few topical accounts and called it CBD experience.

The MCC Code Problem Nobody Talks About

Here’s something most CBD oil merchants never find out until it’s too late. Every merchant account has a Merchant Category Code — an MCC — that tells Visa and Mastercard exactly what your business sells. If your processor assigns you the wrong MCC, every transaction you process looks suspicious to the card networks.

It happens more than you’d think. Some processors use generic ecommerce MCCs to get CBD merchants approved faster. Looks fine on the surface. But when Visa’s risk systems see CBD-related transaction data coming through a code for, say, general retail or health supplements without a CBD-specific approval, it flags the account. No warning. Just a flag that eventually triggers a review or termination.

| Real consequence: An incorrect MCC is a silent termination risk. You’re processing fine, everything looks normal, and then six months in the card network flags an anomaly. Funds frozen, account under review, no explanation. Work with a processor who explicitly confirms your MCC is appropriate for CBD oil before you process a single transaction. |

InclusivePay works directly with acquiring banks to ensure the correct MCC is assigned at account setup. It’s not something merchants should have to think about — but with some processors, it’s a critical question to ask.

The Website Language Trap

This is the number one reason CBD oil merchant accounts get terminated after approval. Not chargebacks. Not compliance issues with COAs. Website language.

Underwriters review your website before approving you. But processors also do ongoing website monitoring after approval. A new product description added by your copywriter, a blog post your social media manager wrote, an updated “about” page — any of it can trigger an automated compliance flag.

Banned phrases — remove from your entire site before applying:

- “Reduces anxiety” or “helps with anxiety”

- “Treats pain,” “relieves pain,” “pain management”

- “Supports sleep” or “helps you sleep”

- “Anti-inflammatory” (unless citing published research without health claims)

- “Medical-grade,” “pharmaceutical-grade,” “clinical-strength”

- “Cures,” “treats,” “prevents,” or “heals” anything

- Any comparison to prescription medications

These phrases don’t have to be on your product pages to get you flagged. They can be in your FAQ, your blog, your meta descriptions, your ad copy, or even your customer reviews if you’re displaying them. Clean your entire site — not just product pages — before you apply, and audit it regularly after approval.

What Underwriters Actually Look At

Most guides give you a document checklist. That’s useful, but it misses what actually determines whether you get approved. Here’s what underwriters are evaluating when they review a CBD oil merchant account application.

- Your website: This is reviewed before anything else. Clean product descriptions, clear return policy, accessible COAs, no health claims, proper age gate if required by your state laws. Underwriters have seen thousands of CBD sites — a non-compliant one is spotted in seconds.

- Your product COAs: Third-party lab, Delta-9 THC at or below 0.3%, within 12 months, covering every SKU. A COA from your manufacturer’s own lab doesn’t count. A COA older than 12 months raises questions. A COA that only covers one product when you sell ten is a red flag.

- Your processing history: Have you processed before? What were your chargeback ratios? A clean processing history is a strong positive signal. A history of elevated chargebacks, even at an aggregator, needs to be explained. No processing history at all is fine for new businesses — it just means more weight is placed on your site and documents.

- Your business history: How long have you been operating? A two-year-old CBD oil business with clean bank statements is a very different risk profile than a two-month-old startup. Neither is disqualifying, but underwriters price for it differently.

- Your volume and growth trajectory: Underwriters set volume limits based on their risk assessment of your business. Understating your volume to get approved and then exceeding it triggers automated review. Be accurate. If you’re growing fast, say so upfront.

Always Run Two Accounts

This is standard operating procedure for any CBD oil brand doing real volume, and almost nobody talks about it.

Run two dedicated merchant accounts with two different acquiring banks simultaneously. Not as a backup you set up after something goes wrong — as a standard configuration from day one. Here’s why.

- If one account has a compliance review triggered, you keep processing on the other Reviews can take weeks. A brand doing $80K/month can’t afford to be offline for three weeks.

- You reduce concentration risk All your revenue through one bank relationship is a single point of failure. Two banks means no single entity has total control over your cash flow.

- Volume balancing If you’re approaching your monthly volume limit on one account, you can route additional transactions through the second. Better than triggering an automated flag.

InclusivePay sets this up for merchants who ask. It’s not complicated — it’s just two applications instead of one, both properly underwritten, both with appropriate MCCs. The peace of mind is worth it.

What You Need to Apply

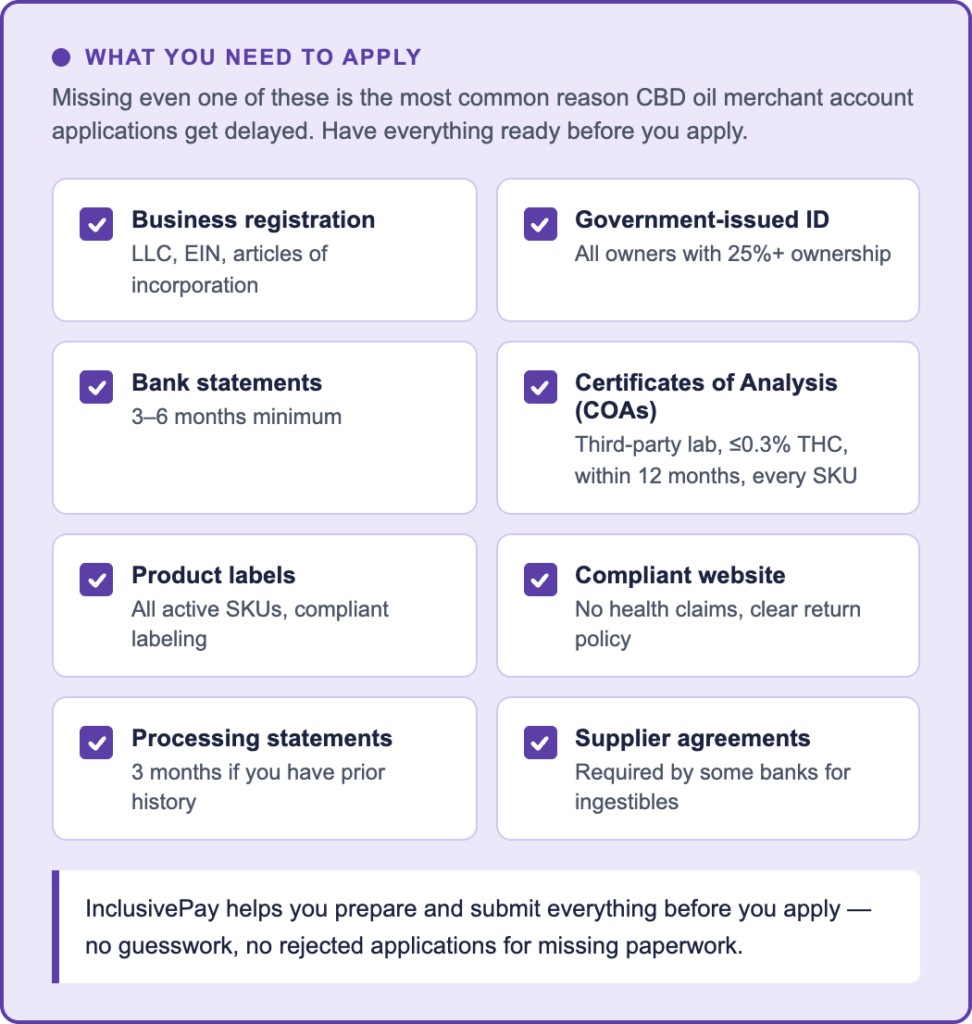

Here’s the complete documentation stack for a CBD oil merchant account application:

- Business registration — LLC, EIN, articles of incorporation

- Government-issued ID for all owners with 25%+ ownership

- 3–6 months of business bank statements

- Certificate of Analysis for every product — third-party lab, Delta-9 THC ≤0.3%, within 12 months

- Product labels for all active SKUs

- Live compliant website — no health claims, clear return policy, COAs accessible

- 3 months of processing statements if you have prior history

- Supplier/manufacturer agreements if requested (some banks require for ingestibles)

For CBD oil and ingestibles specifically: some acquiring banks require supplier agreements confirming your product source and manufacturing standards. Not all do, but having it ready speeds up the process. InclusivePay will let you know upfront what each banking partner requires for your specific product category.

Approval timeline: Pre-approval in 24–48 hours for most CBD oil merchants. Full setup typically 7–10 business days — slightly longer than topicals due to the additional underwriting layer for ingestibles.

FAQs

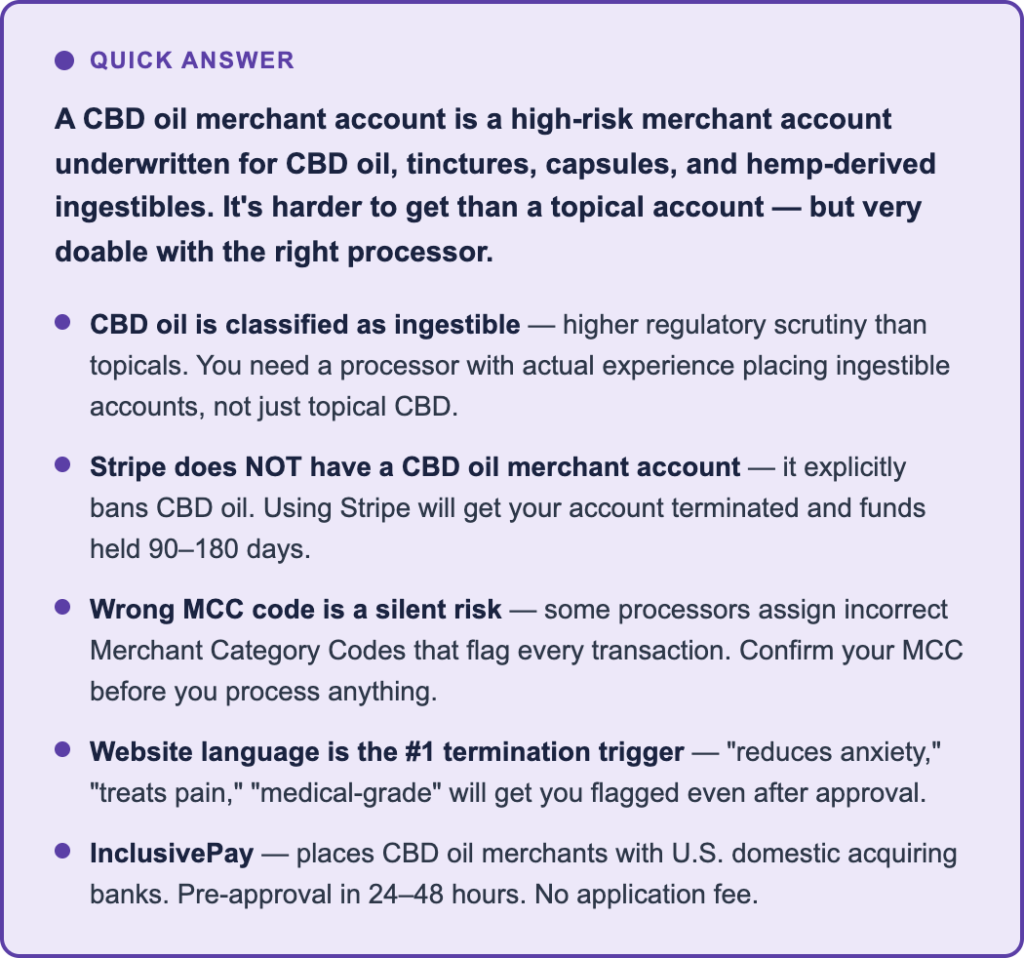

What is a CBD oil merchant account?

A CBD oil merchant account is a high-risk merchant account specifically underwritten for businesses selling CBD oil, tinctures, capsules, gummies, or other hemp-derived ingestibles. It allows you to accept card payments through a U.S. acquiring bank that has reviewed and approved your specific business. See our high-risk merchant account guide for the full explanation.

Does Stripe allow CBD oil sales?

No. Stripe explicitly prohibits CBD and hemp products including CBD oil and all ingestibles. Accounts processing CBD oil through Stripe will be flagged and terminated, funds held 90–180 days. See our guide to what to do when Stripe shuts you down for the full breakdown.

Why is CBD oil considered high risk?

Several compounding factors: the FDA has not approved CBD as a food additive or dietary supplement, creating regulatory uncertainty; ingestibles carry higher chargeback rates than topicals because efficacy claims are harder to satisfy; state laws on CBD ingestibles vary significantly; and most banks have conservative internal policies around health-adjacent products. The classification is about the category’s risk profile — not about your individual business.

How long does CBD oil merchant account approval take?

With InclusivePay, pre-approval for most CBD oil merchants comes within 24–48 hours. Full setup with your gateway live is typically 7–10 business days — slightly longer than topicals due to additional underwriting for ingestibles. Having complete documentation ready upfront is the single biggest factor in approval speed.

What documents do I need for a CBD oil merchant account?

Business registration, owner ID, 3–6 months of bank statements, current COAs for every product, product labels, compliant website. For ingestibles, some banks also require supplier/manufacturer agreements. See our CBD merchant account requirements guide for the complete breakdown.

Can I get a CBD oil merchant account if Stripe or PayPal shut me down?

Yes. Aggregator terminations for CBD are extremely common and don’t disqualify you. The important things are: don’t apply to another aggregator immediately (it worsens your situation), disclose the prior termination when you apply to a specialist, and come with complete documentation. InclusivePay has placed hundreds of merchants who came to us after aggregator shutdowns.

What is a rolling reserve and do I need one?

A rolling reserve is a percentage of your monthly processing volume — typically 5–10% — held by the acquiring bank for 90–180 days as a buffer against chargebacks. It’s standard for CBD oil accounts and you do get the money back. After 12 months of clean history, most merchants can negotiate it down significantly. It’s not a fee — think of it as a security deposit that gets refunded over time.

Does Stripe have a merchant account for CBD oil?

No. Stripe explicitly prohibits CBD oil and all hemp-derived ingestibles in its acceptable use policy. This is one of the most searched questions in the CBD payment space because Stripe’s instant onboarding makes it feel like an option — until your account gets flagged and terminated. Funds are then held for 90–180 days. There is no CBD-specific Stripe program, no workaround, and no appeal process. If you’re currently processing CBD oil through Stripe, stop immediately and get a dedicated merchant account. See our guide to what to do when Stripe shuts you down for the exact steps.

Does InclusivePay support CBD oil, tinctures, and edibles?

Yes. InclusivePay places merchants selling CBD oil, tinctures, capsules, and other hemp-derived ingestibles. See our CBD payment processing page and best CBD processors comparison for full details.

The Bottom Line

CBD oil merchant accounts are absolutely achievable. The merchants who struggle aren’t struggling because their products are unacceptable — they’re struggling because they used the wrong processor type, got assigned the wrong MCC, or had website language that triggered an automated flag.

Get the setup right from the start: dedicated high-risk ISO, correct MCC for ingestibles, compliant website with no health claims, current COAs for every SKU, and ideally two accounts with different banking partners. That stack keeps a CBD oil business processing stably for years.

InclusivePay has been placing CBD oil merchants since 2018. If you want a straight answer on whether we can help with your specific product catalog, reach out here — no application fee, no pressure.

– InclusivePay Merchant Advisory Team | inclusivepay.com | Updated April 2026