Written by the InclusivePay Merchant Advisory Team | Last updated: April 2026

InclusivePay has been placing high-risk merchants since 2018. This guide reflects what we’ve seen work – and what blows up – across hundreds of CBD merchant account applications.

If you’re reading this, there’s a decent chance you just got an email that made your stomach drop. Account terminated. Funds held. No warning, no explanation, no appeal.

Or maybe you’re smarter than that – you’re looking into this before it happens. Either way, here’s what you need to know.

Stripe bans CBD. PayPal bans CBD. Square bans CBD. This isn’t a gray area or a misapplication of policy – it’s explicit, it’s in their terms of service, and it doesn’t matter how compliant your products are. Perfect COAs, clean labels, zero health claims, Farm Bill-compliant THC levels. None of it matters. The category is prohibited, full stop.

What happened to your account wasn’t a mistake. And trying to get back on these platforms isn’t the answer. Here’s what actually is.

What Stripe Actually Says About CBD

Stripe’s acceptable use policy lists “CBD and hemp products” explicitly under restricted businesses. Not implied. Not ambiguous. It’s listed there alongside weapons dealers and payday lenders. If you sell CBD, Stripe was never a legal option.

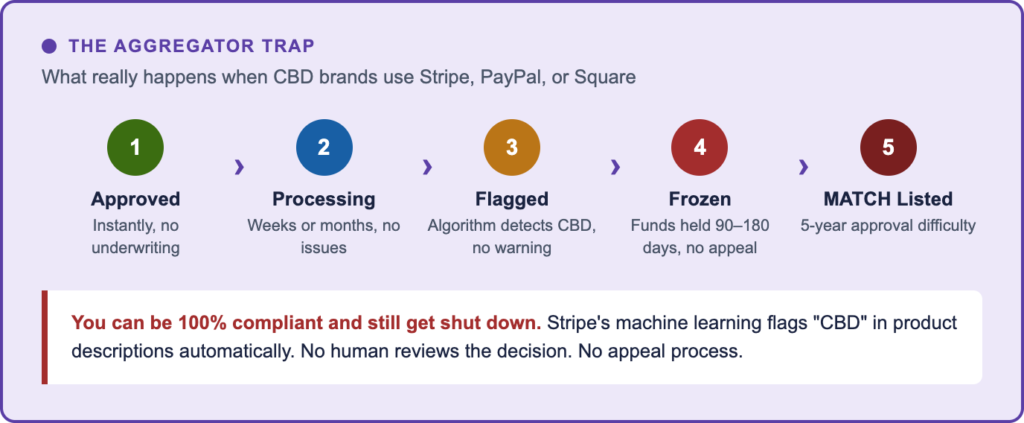

The reason most CBD brands end up on Stripe anyway is the onboarding process. Stripe doesn’t do real underwriting. They approve everyone instantly with automated systems – your business category doesn’t actually get reviewed. You get a green light, you start processing, and their risk algorithms catch up with you weeks or months later. By then you might have tens of thousands of dollars sitting in that account.

When the flag triggers, there’s no human review. No one looks at your COAs or checks your website for health claims. A machine flagged CBD in your product descriptions and the account was frozen. That’s the whole story.

| Real consequence: Stripe holds funds for 90 to 180 days after termination. You cannot withdraw, cannot process new payments, and may be placed on the MATCH list – a database of terminated merchants that makes future approvals harder for up to five years. |

PayPal and Square Are the Same Story

PayPal’s acceptable use policy prohibits “sales of CBD and hemp products.” Same situation – instant onboarding, delayed risk review, eventual termination without notice. PayPal has a documented pattern of holding CBD merchant funds for 180 days and demanding returns for already-delivered products. In one widely-reported case, PayPal classified CBD as “a narcotic” internally and held a merchant’s funds for six months while their business collapsed.

Square’s policy prohibits CBD as well. Square also runs on a shared aggregator model, so the same dynamics apply: fast approval, risk algorithm review, termination when your category gets flagged.

One thing most CBD brands don’t realize about Shopify: Shopify Payments runs on Stripe infrastructure. If you’re using Shopify Payments, you’re using Stripe. The prohibition is identical. You can keep your Shopify storefront – you just need a third-party CBD-friendly payment gateway connected to it.

Why This Keeps Happening – The Aggregator Trap

Stripe, PayPal, and Square are payment aggregators. They don’t give your business its own merchant account. They pull you into a shared pool with millions of other businesses, handle all your transactions through their master accounts, and use automated systems to remove merchants who don’t fit their risk model.

This is why CBD brands keep getting caught. The aggregator model is built for low-risk ecommerce – the kind of business where the main payment risk is the occasional chargeback. CBD is an entire category that card networks scrutinize more heavily, that regulators watch more closely, and that generates different risk signals from day one. Aggregators aren’t set up to handle that. They never were.

Here’s something most payment processing guides won’t tell you: the aggregator trap doesn’t just apply to CBD. If you sell peptides, nootropics or supplements, delta-8, or hemp flower, you’re in the same boat. The same automated flags. The same termination risk. The same fund holds. The category gets you, even when your individual business is completely clean.

Aggregator vs. Dedicated Merchant Account: What’s Actually Different

| Feature | Stripe / PayPal / Square | InclusivePay |

| CBD allowed? | No — prohibited in ToS | Yes, with proper documentation |

| Underwriting | None — auto-approved instantly | Full, before approval |

| Account stability | Frozen without warning | Stable, long-term |

| Funds held on termination | 90–180 days | Not applicable |

| Volume cap | $5K–$20K/month | $100K+/month |

| Shopify / WooCommerce | Blocked for CBD | Supported |

| Chargeback support | None | Monitoring and tools |

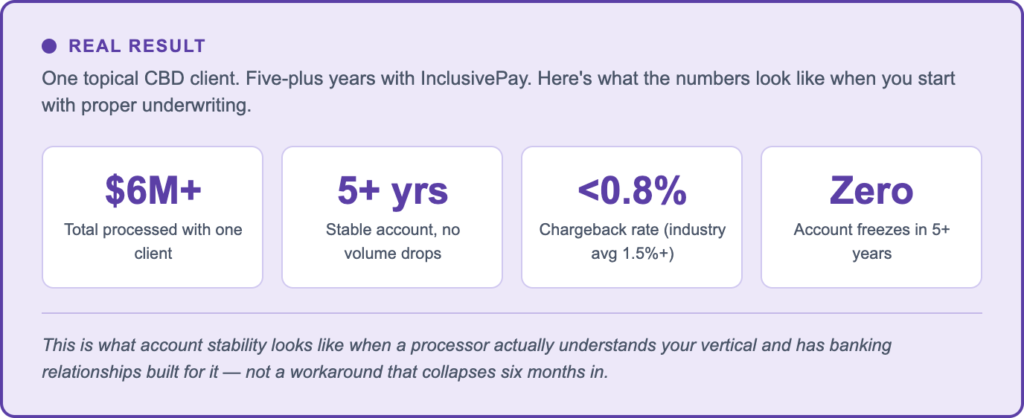

| REAL RESULTOne topical CBD brand has processed over $6M with InclusivePay across 5+ years. No volume drops. Chargebacks held under 0.8%. Never frozen. |

That kind of stability doesn’t happen by accident. It happens because the account was properly underwritten before the first transaction, placed with a bank that specifically supports this category, and actively managed afterward. That’s the difference between a dedicated merchant account and an aggregator workaround.

What to Do Right Now If Your Account Was Frozen

If your Stripe, PayPal, or Square account is currently frozen, here’s the order of operations.

Step 1: Don’t apply to another aggregator.

The instinct when one account shuts down is to immediately apply somewhere else – Stripe’s competitor, Square’s competitor, whoever. Do not do this. If you process even a small amount on a new aggregator account in the same category before getting flagged again, you increase your MATCH list risk significantly. Stop the cycle.

Step 2: Get your documentation together.

While you’re waiting for funds to release, gather everything: transaction logs from the frozen account, termination notice in writing if you received one, all bank statements, current COAs for your products, and your business registration documents. You’ll need all of this for your next application, and having it ready speeds up approval.

Step 3: Check your MATCH list status.

Not all aggregator terminations result in a MATCH listing, but some do – especially if you had elevated chargebacks at the time of termination. Contact us and we can help determine your status before you apply anywhere. Being MATCH-listed doesn’t disqualify you from a dedicated merchant account, but it changes what you need to prepare.

Step 4: Apply through a specialist, not another aggregator.

A dedicated high-risk ISO – like InclusivePay – actually underwrites your business before approval. They review your products, your compliance posture, your site, your processing history. See our full guide to CBD payment processing and comparison of the best CBD processors to understand what to look for.

Step 5: Set up backup processing while you wait.

Even after approval, running two dedicated merchant accounts with different banking partners is smart. If one has an issue – and it’s rare, but things happen – the other keeps processing. Don’t put your entire revenue on one account again.

How to Get a CBD Merchant Account That Won’t Freeze

Getting approved isn’t complicated if you come prepared. Here’s what the process actually looks like with InclusivePay.

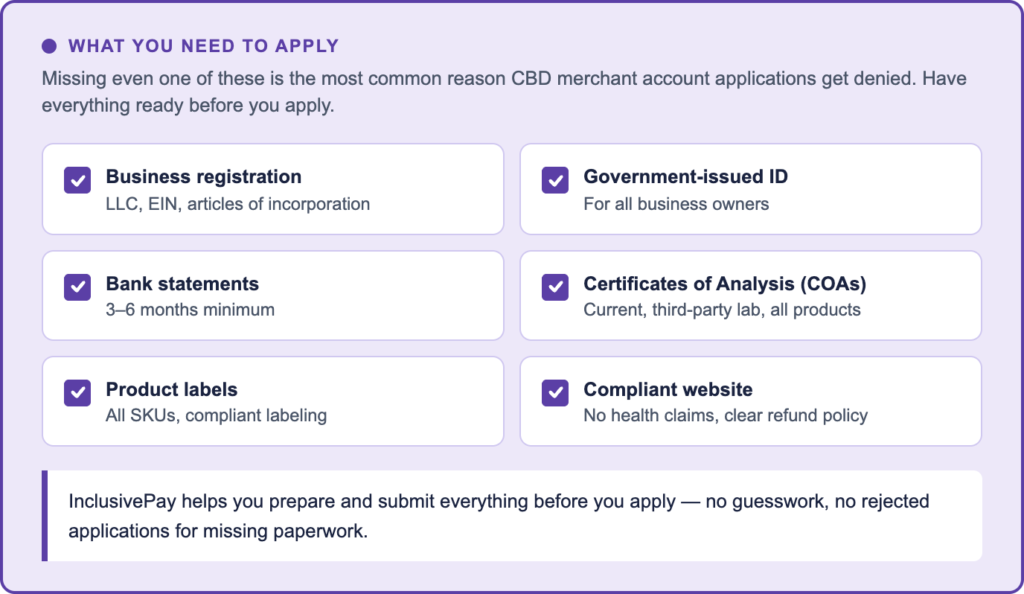

What you’ll need:

- Business registration documents (LLC, EIN, articles of incorporation)

- Government-issued ID for all owners with 25% or more ownership

- 3–6 months of business bank statements

- Current Certificates of Analysis (COAs) for all products – third-party lab, within 12 months

- Product labels for all active SKUs

- Live, compliant website with return policy – no health claims

Your website is reviewed as part of underwriting. Remove any language that could be interpreted as a disease treatment claim – even subtle phrases like “reduces anxiety” or “supports sleep” can slow an application. If you’re not sure what counts, ask us before you apply.

Timeline: Pre-approval within 24 to 48 hours for most CBD merchants. Full setup in 5 to 7 business days. Gateways: Authorize.Net and NMI, compatible with WooCommerce and Shopify.

Platform-Specific Setup: Shopify, WooCommerce, BigCommerce

Shopify: Disable Shopify Payments – it runs on Stripe and will shut you down. Connect a third-party CBD-friendly gateway. InclusivePay integrates via approved gateways so you keep your storefront.

WooCommerce: One of the better platforms for CBD – open-source and supports third-party gateway plugins. InclusivePay connects via Authorize.Net or NMI. See our WooCommerce CBD gateway guide for full setup details.

BigCommerce: More flexible than Shopify on payment policy. Allows third-party gateway integration and doesn’t restrict CBD at the platform level. You still need a dedicated high-risk merchant account. The platform flexibility just means fewer hoops on the storefront side.

FAQs

Does Stripe allow CBD payments?

No. Stripe explicitly prohibits CBD and hemp products in its acceptable use policy. Even if your account is initially approved – which happens because Stripe doesn’t do real-time underwriting – it will eventually be flagged and terminated. Your funds will be held for 90 to 180 days. Do not use Stripe for CBD.

Does PayPal allow CBD?

No. PayPal’s acceptable use policy prohibits CBD and hemp products. PayPal has a documented history of holding CBD merchant funds for 180 days and demanding returns on already-delivered orders. It is not a viable option for CBD businesses.

Does Square allow CBD sales?

No. Square’s acceptable use policy prohibits CBD. Square is a payment aggregator and uses the same automated risk model as Stripe and PayPal – fast approval, delayed review, termination when the category is flagged.

What if my CBD account was frozen by Stripe or PayPal – can I get my money back?

Yes, eventually. Stripe and PayPal typically hold funds for 90 to 180 days after account termination. You will get the money back assuming no active dispute resolution depletes the reserve. Do not continue processing on another aggregator while waiting – this can complicate or extend the hold. Contact us to talk through your specific situation.

Can I use Shopify Payments for CBD?

No. Shopify Payments runs on Stripe infrastructure and carries the same CBD prohibition. Disable Shopify Payments and connect a third-party CBD-friendly gateway. InclusivePay integrates with Shopify via approved gateways. See our WooCommerce CBD gateway guide for platform setup details.

What’s the difference between a payment aggregator and a dedicated merchant account?

A payment aggregator (Stripe, PayPal, Square) pools your transactions with thousands of other merchants under one master account and monitors risk with automated algorithms. A dedicated merchant account is individually underwritten – the bank has reviewed your specific business and agreed to support it before you process anything. That prior agreement is what makes the account stable. Aggregators were never built for high-risk categories. See our high-risk merchant account guide for the full breakdown.

How fast can InclusivePay get me approved?

Pre-approval for most CBD merchants within 24 to 48 hours. Full setup with gateway live in 5 to 7 business days, assuming documentation is in order. No application fee.

Do peptide and nootropic sellers face the same problem?

Yes. Peptides and nootropics face the same aggregator prohibitions and the same termination risk as CBD. These categories are classified as high-risk due to regulatory gray areas, health-adjacent claims, and elevated dispute rates. InclusivePay works with both. See our peptide merchant account page and nutraceutical merchant account page for details.

What if I was placed on the MATCH list?

A MATCH listing makes future approvals harder but doesn’t permanently disqualify you from getting a dedicated merchant account. It depends on the reason for the listing. Aggregator terminations in prohibited categories (CBD, hemp) are different from terminations for fraud or excessive chargebacks. Contact us with your history and we’ll give you a straight answer on your options.

The Bottom Line

Stripe, PayPal, and Square were never built for CBD. The fact that they let you through the door doesn’t change that. The aggregator model approves first and terminates later, and in prohibited categories, termination is always coming. It’s not a matter of if – it’s a matter of when and how much money you lose in the process.

The fix is a dedicated merchant account with a processor that actually does underwriting for your vertical. Not another aggregator workaround. Not a gray-area payment method that works until it doesn’t. A real account with a named U.S. domestic bank that knows what you sell and agreed to support you before your first transaction.

InclusivePay has been placing CBD and alternative health merchants since 2018. If you want to talk through your situation before applying, reach out through the contact page – no application fee, no pressure, just a straight answer on whether we can help.

– InclusivePay Merchant Advisory Team | inclusivepay.com | Updated April 2026