Written by the InclusivePay Merchant Advisory Team | Last updated: April 2026

InclusivePay has been placing high-risk merchants since 2018. This guide reflects what we’ve seen work – and what blows up – across hundreds of applications in CBD, hemp, peptides, nootropics, and other alternative health verticals.

If you’re reading this, there’s a decent chance you just got an email from Stripe, PayPal, or Square that made your stomach drop. Or maybe you’re smarter than that – you’re doing the research before you get shut down. Either way, you’re in the right place.

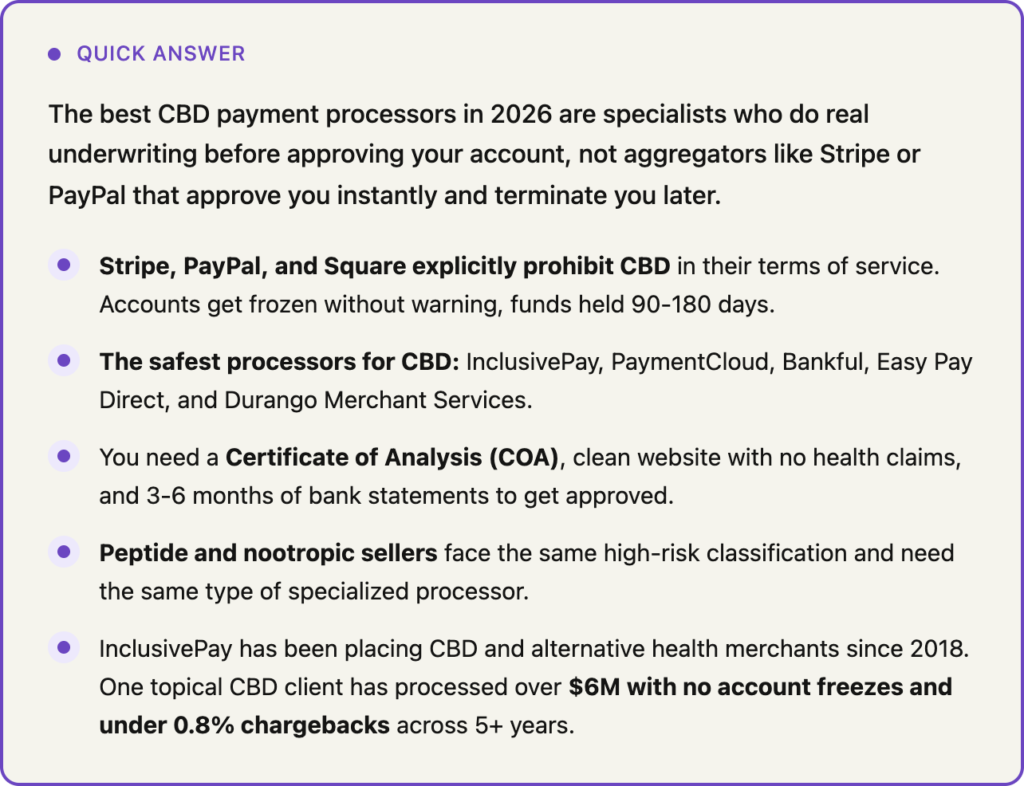

Here’s the truth nobody tells CBD brands upfront: finding a payment processor that won’t eventually freeze your account isn’t about compliance. You can have perfect COAs, clean labels, and zero health claims on your site – and still wake up to frozen funds and a termination email. We’ve seen it happen to brands doing $50K/month and brands doing $500K/month. The processor isn’t the problem. Using the wrong type of processor is.

This guide breaks down the best CBD and hemp payment processors in 2026, what separates a real high-risk specialist from a risky workaround, and what you actually need to get approved and stay approved. We also cover why the same payment challenges now apply to peptide sellers, nootropic brands, and other alternative health businesses – and what to do about it.

Why CBD and Hemp Brands Keep Getting Shut Down

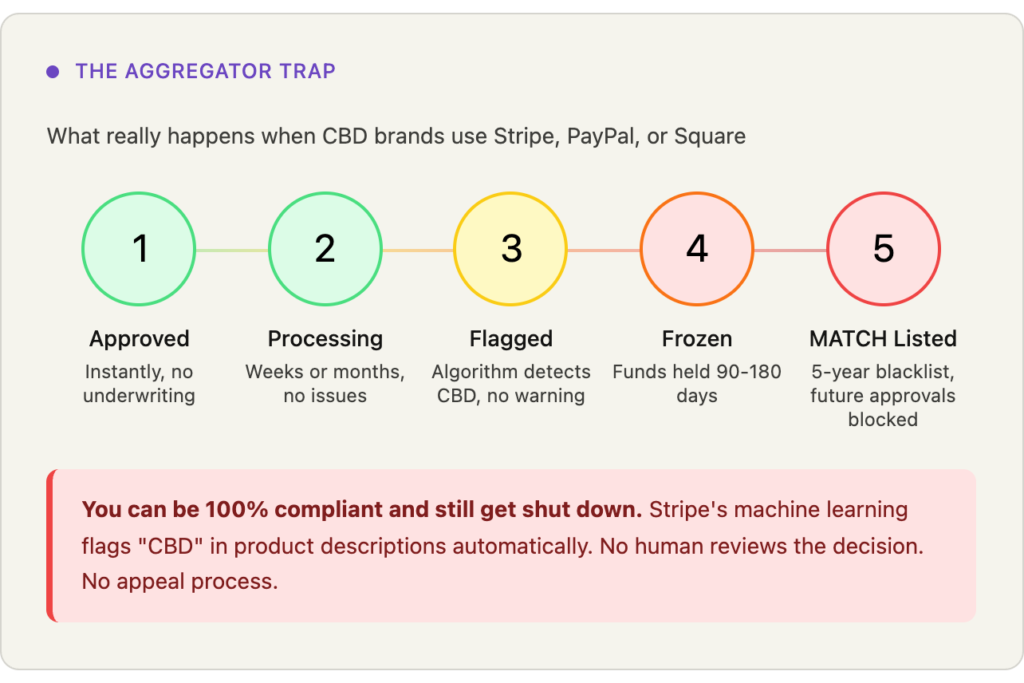

Let’s start with the part that confuses most merchants. You sign up for Stripe. You get approved in seconds. You start processing. Everything’s fine for two weeks, six weeks, maybe three months. Then one day: account frozen, funds held, no warning, no appeal.

This isn’t bad luck. It’s the aggregator trap, and it catches the vast majority of CBD brands at some point.

Stripe, PayPal, and Square are payment aggregators. They don’t underwrite your business before approving you. They pull you into a shared merchant pool with thousands of other businesses, approve you instantly with automated systems, and let their risk algorithms sort things out later. When those algorithms flag your products – and they will, because CBD is explicitly prohibited in Stripe’s acceptable use policy – your account gets frozen without a human ever reviewing your business.

Real consequence: Funds are typically held for 90 to 180 days after termination. You cannot withdraw, cannot process new payments, and may be placed on the MATCH list – a database of terminated merchants that follows you for five years and makes future approvals much harder.

The other thing nobody warns you about: you don’t have to be doing anything wrong for this to happen. A sudden spike in volume, a product description with a wellness phrase an algorithm doesn’t like, a chargeback ratio that ticks up during a busy season – any of these can trigger an automated review and account freeze. Clean businesses get shut down constantly.

Aggregator vs. High-Risk Specialist: What’s the Actual Difference?

This is the most important thing to understand before you choose a processor. Not all processors are built the same way – and the difference determines whether your account is stable or a ticking clock.

| Feature | Aggregator (Stripe / PayPal / Square) | High-Risk Specialist (InclusivePay) |

| Underwriting | None – auto-approved instantly | Full underwriting before approval |

| CBD allowed? | Prohibited in ToS | Yes, with proper documentation |

| Account stability | Frozen without warning | Stable with ongoing support |

| Funds held on termination | 90-180 days | Not applicable |

| MATCH list risk | High | Low when properly underwritten |

| Shopify / WooCommerce support | Limited or blocked for CBD | Supported via approved gateways |

| Chargeback support | None | Monitoring and prevention tools |

| Who it’s built for | Low-risk businesses | CBD, hemp, peptides, alternative health |

Best CBD and Hemp Payment Processing Companies in 2026

Here are the processors that actually work for CBD and hemp businesses. Each has different strengths – the right choice depends on your volume, platform, and product catalog.

1. InclusivePay – Best for CBD Ecommerce and Alternative Health Verticals

Best for: CBD ecommerce brands, hemp sellers, peptide businesses, nootropic brands, subscription models, Shopify and WooCommerce stores

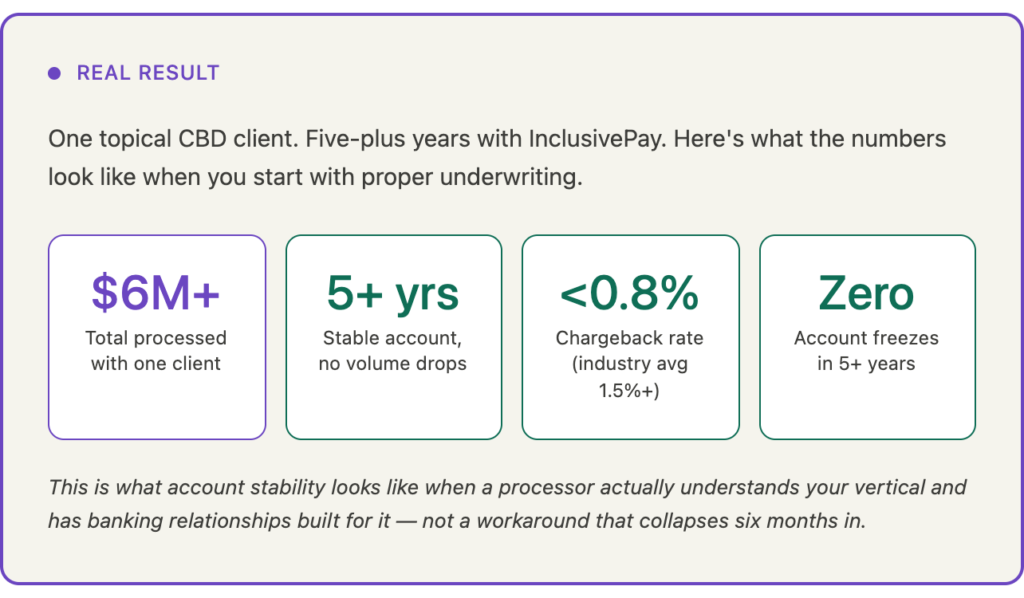

InclusivePay has been placing high-risk merchants since 2018, with a specific focus on CBD, hemp, and alternative health verticals. Unlike brokers who hand you off to a bank and disappear, InclusivePay stays involved after approval – because account stability over time is what actually matters.

Real result: One topical CBD brand has processed over $6M with InclusivePay across 5+ years. No volume drops. Chargebacks held under 0.8%. Never frozen.

That kind of long-term account health is rare in this industry. Most CBD brands cycle through processors every 12 to 18 months. The difference is proper underwriting upfront and a processor that has actual banking relationships built for this category – not a workaround that gets quietly shut down six months in.

InclusivePay also supports verticals beyond CBD that face the same payment processing challenges: peptides, nootropics, delta-8, hemp flower, and other alternative health products. If your form lead pool looks like ours – peptide sellers and nootropic brands knocking on the door – this matters.

Key features:

- CBD and hemp merchant accounts with proper underwriting

- Shopify, WooCommerce, and ClickFunnels integration

- Supports $100K+/month processing volume

- 48-72 hour pre-approval, 5-7 day full setup

- Chargeback monitoring and fraud prevention tools

- Covers peptides, nootropics, delta-8, and other alternative health verticals

- No application fee, no volume lock, no frozen funds policy

- U.S.-based team with 8+ years in high-risk payments

Approval timeline: 48-72 hours for pre-approval, 5-7 business days for full setup with documentation in order.

2. PaymentCloud – Best for Broad High-Risk Coverage

Best for: CBD brands who need options across multiple banking relationships, dispensaries (hemp-only), businesses with complex product catalogs

PaymentCloud is one of the more established names in high-risk processing and works with a network of banking partners to find the right fit for each merchant. They’re not specialists in CBD the way InclusivePay is, but their breadth of banking relationships can be useful for businesses that have had previous terminations or are in gray-area product categories.

Key features:

- Multiple banking partner network

- CBD and hemp merchant account approval

- Credit, debit, and ACH processing

- Payment gateway integration

- Fraud protection tools

Worth knowing: PaymentCloud acts more as a broker, matching you to banks in their network. Stability can vary depending on which bank you end up with. Good for getting approved; less consistent on long-term account health.

3. Bankful – Best for WooCommerce CBD Stores

Best for: WooCommerce-first CBD brands, merchants who need a clean plugin integration

Bankful focuses specifically on high-risk industries and has solid WooCommerce integration. If your store runs on WooCommerce and you’ve struggled to find a gateway that plays nicely with your setup, Bankful is worth evaluating. They’ve built their infrastructure around industries that mainstream processors avoid.

Key features:

- WooCommerce payment gateway plugin

- CBD and supplement merchant support

- Chargeback monitoring

- Fraud detection tools

4. Easy Pay Direct – Best for High Volume CBD Brands

Best for: Established CBD brands processing $100K+/month, subscription businesses, high-ticket product catalogs

Easy Pay Direct has been in the high-risk space for years and uses a load-balancing system that spreads transactions across multiple merchant accounts. This can help with volume stability and reduce the risk of any single account triggering a review. Better fit for an established brand than a newer business.

Key features:

- Load-balanced processing across multiple accounts

- Recurring billing and subscription support

- CBD and hemp merchant account approval

- Shopify and WooCommerce compatible

- Chargeback prevention tools

Worth knowing: Onboarding can be slower than other options. Better suited for established brands with processing history than new launches.

5. Durango Merchant Services – Best for International CBD Sales

Best for: CBD brands selling internationally, businesses needing multi-currency support

Durango has a long track record in high-risk merchant services and handles international transactions well. If a significant portion of your revenue comes from outside the US, they’re worth including in your evaluation. Domestic-only brands will likely find better fits above.

Key features:

- International and offshore merchant account support

- Multi-currency processing

- CBD and high-risk merchant experience

- Fraud and chargeback tools

CBD Payment Processing by Platform

Shopify

Shopify Payments (which runs on Stripe infrastructure) does not support CBD. You’ll need a third-party payment gateway. InclusivePay integrates via approved third-party gateways so you keep your Shopify storefront while processing through a CBD-friendly merchant account. See our full guide on Shopify CBD payment processing for setup details.

WooCommerce

WooCommerce is actually one of the better platforms for CBD because it’s open-source and supports a wide range of third-party gateway plugins. Most high-risk processors can connect via plugin or API. InclusivePay, Bankful, and NMI all have WooCommerce-compatible setups. See our WooCommerce CBD gateway guide for a full breakdown.

BigCommerce

BigCommerce allows third-party gateway integration and is generally more CBD-friendly than Shopify in terms of platform policy. You’ll still need a dedicated high-risk merchant account – the platform flexibility just means fewer hoops on the storefront side.

Beyond CBD: Payment Processing for Peptides, Nootropics, and Alternative Health

Here’s something most payment processing guides won’t tell you: if you sell peptides or nootropics, you’re dealing with the exact same payment processing challenges as CBD brands. Sometimes worse.

Why peptides are high-risk: Peptides occupy a genuinely gray regulatory space. Many are sold legally as research chemicals but are increasingly scrutinized by banks and card networks due to their proximity to prescription drug categories, evolving FDA positioning, and higher-than-average dispute rates. Mainstream processors won’t touch them, and many high-risk processors won’t either.

Why nootropics are high-risk: The same story applies. Products marketed for cognitive enhancement attract regulatory attention, and processors flag anything that could be interpreted as a health claim. Combined with subscription models (common in this space) and high ticket sizes, nootropic brands are routinely denied by aggregators and many high-risk specialists.

InclusivePay works with both categories. If your form submissions are coming from peptide or nootropics businesses, that’s a signal the demand is there – and so is the gap in the market for processors who actually understand these verticals.

How to Get Approved for a CBD Merchant Account

Getting approved isn’t complicated if you work with the right processor and come prepared. Here’s what the process actually looks like.

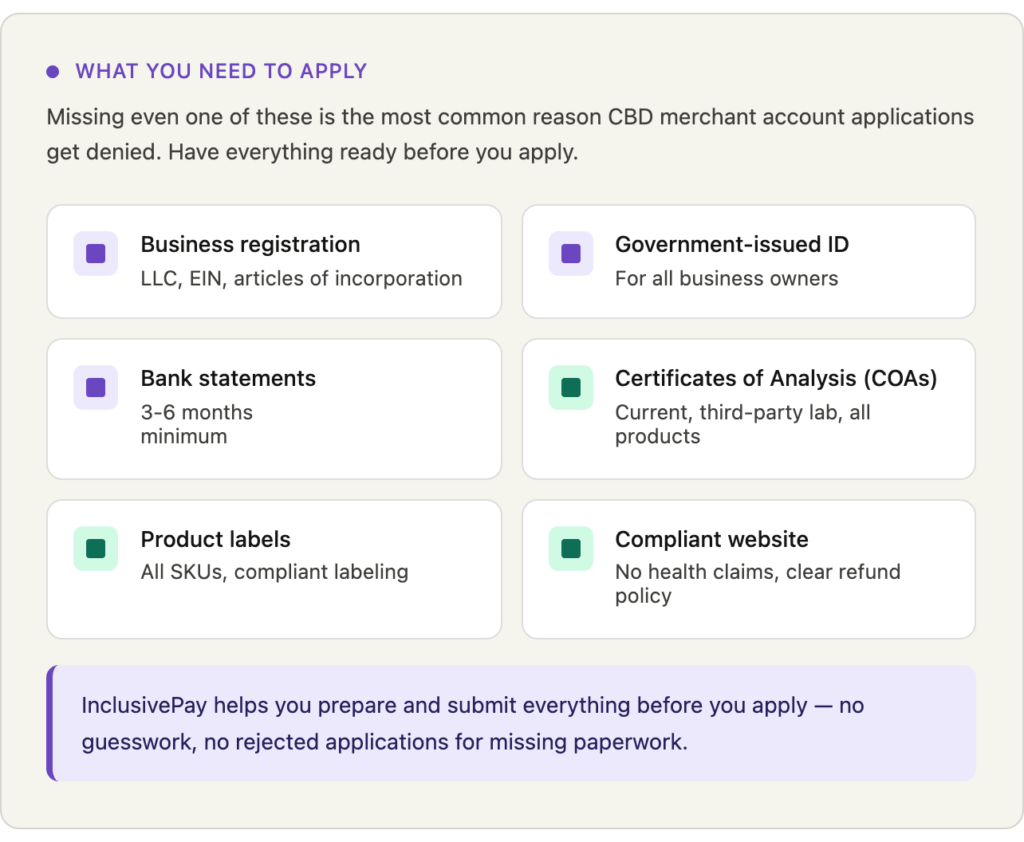

Step 1: Get your documents ready before you apply.

Most denials happen because merchants apply without a complete documentation stack. Have these ready:

- Business registration documents (LLC, EIN, articles of incorporation)

- Government-issued ID for all owners

- 3-6 months of business bank statements

- Processing statements if you have prior history

- Certificates of Analysis (COAs) for all products

- Product labels

- Live, compliant website with clear return/refund policy

Step 2: Clean up your website.

Underwriters look at your site before approving you. Anything that looks like a health claim – even subtle language like ‘reduces anxiety’ or ‘supports sleep’ – can kill an application. Remove any FDA-prohibited claims, make sure your COAs are linked or accessible, and confirm your checkout flow is clean.

Step 3: Apply through a specialist, not an aggregator.

The most common mistake is applying to Stripe or PayPal after getting rejected elsewhere. It doesn’t work, and it can get you placed on the MATCH list if you process even a small amount before getting flagged. Apply through a processor that does actual underwriting for your vertical.

Step 4: Be honest about your volume and product catalog.

Underwriters will find out what you sell and how much you process. If you understate your volume to get approved and then exceed it, you risk triggering a review or freeze. Be accurate from the start and work with a processor who knows your category.

Step 5: Maintain compliance ongoing.

Getting approved is step one. Keeping your account stable means staying on top of COA updates, watching your chargeback ratio (keep it under 1%, ideally under 0.8%), avoiding sudden volume spikes without advance notice to your processor, and keeping your site clean of prohibited language.

FAQs

Can Stripe process CBD payments?

No. Stripe explicitly prohibits CBD in its acceptable use policy. Even if your account is initially approved – which can happen because Stripe doesn’t do real-time underwriting – it will eventually be flagged and terminated. Your funds will be held for 90-180 days. Do not use Stripe for CBD.

What happens if my CBD merchant account gets shut down?

First, don’t apply to another aggregator. Gather your transaction logs, processing statements, and termination notice in writing. Check whether you’ve been placed on the MATCH list (a high-risk merchant database that affects future approvals). Then apply through a high-risk specialist who can review your documentation and underwrite your business properly. If you’re MATCH-listed, it’s not a permanent ban – specialists can still work with you.

How long does CBD merchant account approval take?

With InclusivePay, pre-approval typically comes within 48-72 hours. Full setup with banking in place is usually 5-7 business days, assuming your documents are in order. Applications without COAs or incomplete bank statements take longer.

Do I need a COA to get approved?

Yes. A Certificate of Analysis from a third-party lab is non-negotiable for CBD merchant account approval. It needs to confirm your products contain 0.3% THC or less (for hemp-derived CBD) and should be current – most underwriters want COAs within the last 12 months. Missing or outdated COAs are one of the most common reasons applications are rejected.

Can I use PayPal as a backup payment option for CBD?

Technically some merchants have done this for a period of time, but PayPal prohibits CBD in its acceptable use policy. The risk of a sudden freeze and fund hold is the same as with Stripe. It’s not a reliable backup. A better approach is to have two dedicated high-risk merchant accounts with different banking partners, so if one has an issue the other keeps processing.

What’s the difference between a payment gateway and a merchant account for CBD?

A merchant account is the actual bank-level relationship that holds your funds and enables you to accept card payments. A payment gateway is the software layer that connects your storefront to that merchant account. For CBD, you need both – and you need both to be CBD-friendly. Some processors provide the gateway only and require you to already have a merchant account; others (like InclusivePay) set up the full stack.

Does InclusivePay support peptide sellers?

Yes. InclusivePay works with peptide businesses. Peptides fall into the same high-risk category as CBD due to regulatory gray areas and elevated dispute rates. If you’ve been rejected by other processors, contact us for a consultation – peptides require a more detailed underwriting conversation but approval is possible with the right documentation.

Can I get approved if I also sell nootropics alongside CBD?

Yes, mixed catalogs are something InclusivePay regularly handles. The key is full transparency during underwriting – list all product categories you sell or plan to sell. Applications that hide product diversity tend to have more account stability issues later.

What if I was previously shut down by Stripe or PayPal?

A prior shutdown doesn’t disqualify you from getting a high-risk merchant account, as long as you weren’t placed on the MATCH list for reasons like fraud or excessive chargebacks. Even MATCH-listed merchants have options. The important thing is to be upfront about your history and come to the application with solid documentation. Processors that specialize in CBD have seen every variation of this situation.

The Bottom Line

Most CBD and hemp brands don’t fail because of a bad product or weak marketing. They fail because their payment processing collapses at the worst possible moment – during a launch, a seasonal spike, or right after they’ve scaled ad spend.

The processors on this list have actual banking relationships built for this category. They underwrite your business before you start processing, not after. That single difference – underwriting upfront versus automated approval with delayed termination – is what separates a stable payment setup from a ticking clock.

If you’re starting fresh, do it right the first time. If you’ve already been shut down, don’t make the same mistake twice. And if you’re selling peptides or nootropics and getting turned away everywhere, the problem isn’t your business – it’s that most processors haven’t built the relationships to serve your vertical yet.

InclusivePay has been in this space since 2018. If you want to talk through your situation before applying, reach out through the contact page – no application fee, no pressure, just a straight answer on whether we can help.

– InclusivePay Merchant Advisory Team | inclusivepay.com | Updated April 2026