- Trusted by 500+ CBD & Hemp Brands

High Risk Merchant Account Payment Processing for CBD and High-Risk Brands

We help serious operators get stable, domestic merchant accounts through a high risk payment processor without the inflated rates, shady workarounds, or surprise shutdowns.

Get a stable merchant account

No application fee. We tell you honestly whether you’re approvable before you submit anything.

8+ Years

In High-Risk Payments

$100K+/mo

Topical CBD Client 5+ Years

Fast Approval

For Compliant Brands

U.S.-Based

Team That Gets It

A high risk merchant account is a dedicated payment processing account underwritten by a U.S. acquiring bank that has specifically agreed to support your product category. CBD, hemp, nutraceuticals, peptides, vape, supplements, adult, and coaching are all classified as high risk by card networks — which means Stripe, PayPal, Square, and Shopify Payments will approve you instantly and shut you down when their automated systems flag your transactions.

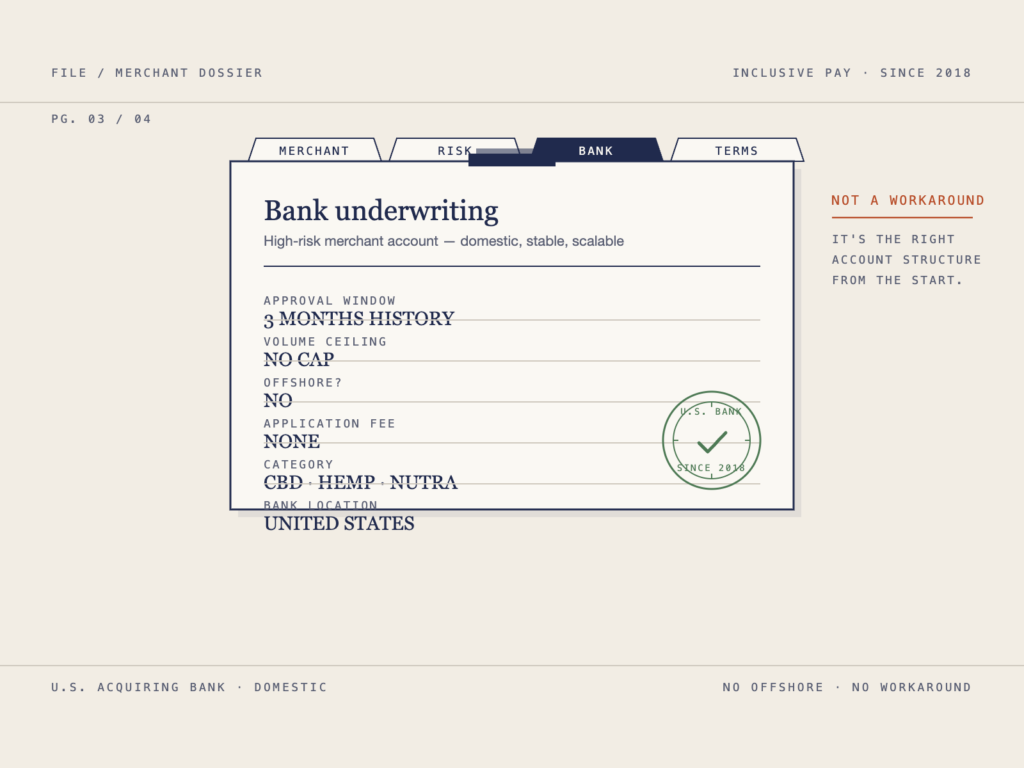

The fix is not a workaround. It is the right account structure from the start. Approval requires 3 months of processing history. Accounts over $100K monthly volume require two years of tax returns or audited financials. InclusivePay is a U.S.-based ISO that has placed high-risk merchants with stable domestic acquiring banks since 2018.

No application fee. No offshore workarounds. No volume caps that hold you back once you start scaling.

2018

Placing high-risk

merchants since

500+

CBD and alt-health

brands placed

<0.8%

Chargeback rate,

top CBD client

0

Account freezes

for that client

Why High-Risk Payment Processing Is Different

You built a real business in a category the aggregators won’t serve. CBD topicals. Supplements. Peptides. Hemp. Nootropics. Your products are compliant, your labeling is clean, your COAs are current. Then Stripe froze your account anyway — or Square terminated you without a word. That is not a compliance failure. That is what happens when you use a processor that was never built for your category.

“High-risk” is a banking classification, not a judgment about your business. Card networks like Visa and Mastercard assign every merchant to a category based on chargeback patterns, regulatory exposure, and product claim sensitivity. CBD, hemp, nutra, peptides, vape, adult, coaching, SaaS subscriptions, travel, and firearms all fall into the high-risk bucket. It does not matter how clean your operation is. If you sell in one of these categories, banks price risk into your account — and the right banking structure matters more than any other single decision you will make about your business.

The structural problem is the aggregator model. Stripe, PayPal, Square, Shopify Payments, and WooPayments are payment aggregators. They approve everyone instantly with no individual underwriting, pool thousands of merchants under one master account, and use automated risk algorithms to remove anyone whose transactions pattern-match a flagged category. They are designed to be frictionless for coffee shops and SaaS startups — not for the businesses Visa has classified as high-risk. When the algorithm sees “CBD” or “peptide” or “nootropic” in your product descriptions, the clock starts ticking on your account regardless of whether you are doing anything wrong.

Ready to apply?

No application fee. We review your setup and tell you which pathway fits your business before you submit anything.

Approved immediately with no underwriting — then shut down weeks or months later when transactions are reviewed

Funds frozen for 90 to 180 days with no explanation and no appeal process

MATCH listing risk — five years of harder approvals if your termination triggers it

No human review, no appeal — automated flagging, automated termination

A dedicated high-risk merchant account works differently. The acquiring bank has reviewed your specific business — your products, your volume, your compliance posture — and made an underwriting decision to support you. That approval is durable in a way that instant aggregator approvals never are. It is the difference between a bank that knows what you sell and one that approved you before reading a single line of your product descriptions.

High-Risk Industries We Place

Every high-risk vertical has its own underwriting considerations — different claim sensitivities, different chargeback patterns, different banking requirements. We do not pretend one-size-fits-all works. The pages below cover the category-specific details.

CBD & Hemp

Topicals, tinctures, gummies, skincare, pet products, hemp flower, delta-8 and delta-10. Federally legal under the 2018 Farm Bill, banned by every major aggregator.

Nutraceuticals & Supplements

Vitamins, nootropics, weight loss, pre-workout, herbal adaptogens, greens, sleep, immune. Subscription auto-ship supported when structured correctly.

Peptides

Research-only ecommerce and LegitScript-certified clinic models. Both pathways supported. LegitScript is not always required.

Cannabis (Compliant Ops)

State-legal dispensary and compliant cannabis ecommerce. Underwriting requirements are tighter — contact us before applying.

Vape & E-Cigarettes

Nicotine vape, disposables, pods, hardware. Strict PACT Act compliance required. Age-verification built into checkout.

Adult, Coaching & Other High-Risk

Adult products and services, high-ticket coaching, SARMs, and other categories flagged by card networks. Every applicant reviewed individually.

Each vertical has different approval requirements and different typical rate structures. Use the category pages above for the specifics that matter for your business, or contact us directly if your category is not listed.

Aggregators vs. InclusivePay for High-Risk Processing

- Prohibited — CBD, nutra claims flagged, peptides flagged, vape restricted

- Underwritten for hemp, CBD, nutra, peptides, and more

- Instant approval, no review until transactions flag

- Real underwriting before approval

- $5K – $20K/month before review triggers shutdown

- $100K+ monthly volume supported

- Instant — then terminated weeks or months later

- 48–72 hour pre-approval, full setup 5–7 days

- High — 90 to 180 days is standard when flagged

- Structurally stable — risk priced into underwriting

- None — no dedicated account support

- Alerts, descriptor strategy, ongoing monitoring

- Limited — Shopify Payments and WooPayments block high-risk

- Shopify, WooCommerce, BigCommerce, ClickFunnels, POS, custom

- None

- COA, label, and KYC document prep

- Algorithmic monitoring — subject to sudden review

- Underwritten account + ongoing management

- Varies

- None

$2M/month CBD brand — five-plus years with us, no freezes, chargebacks well under threshold. $30K/month peptide brand — five-plus years, zero issues, zero terminations. Topical CBD brand — $6M+ processed across 5+ years, under 0.8% chargebacks, never frozen. None of this is possible on Stripe, Square, PayPal, or Shopify Payments. It is what a properly underwritten merchant account with active account management produces.

What InclusivePay Provides

InclusivePay is a U.S.-based ISO — an Independent Sales Organization — registered with the major card networks. We work directly with domestic acquiring banks to place your business in a properly underwritten high-risk merchant account. You know who holds your account. We manage the relationship to keep it stable.

Domestic high-risk merchant account

Underwritten by U.S. acquiring banks that specifically accept your product category. You know the bank holding your account. No offshore routing, no opaque pooling, no workarounds.

Gateway setup via Authorize.Net or NMI

Both integrate with Shopify, WooCommerce, BigCommerce, ClickFunnels, and custom cart setups. We configure the billing descriptor to match your store name and reduce friendly fraud chargebacks from day one.

$100K+ monthly volume supported

No arbitrary volume caps. Scale without triggering the "unusual volume" review that kills aggregator accounts. Ongoing underwriting conversations with the bank as you grow.

Subscription and recurring billing

Fully supported for auto-ship, monthly subscriptions, and recurring memberships when structured correctly. Free-trial-to-subscription models are prohibited by card networks — we help you restructure to what is allowed.

Ongoing account management

We stay involved after go-live. Reachable before you launch a campaign, add a product category, or scale volume. Proactive outreach when something changes that could affect your account.

Support across adjacent verticals

Most brands are not single-category. A CBD brand adds a supplement SKU. A supplement brand tests a peptide. A peptide brand launches a clinic arm. One relationship, multiple verticals — each underwritten correctly.

Chargeback management via ClearSale

Chargebacks are death in this niche. We partner with ClearSale — the industry standard for fraud prevention and chargeback resolution — plus 3DS, AVS, descriptor strategy, and representment support. This combination is what keeps our top clients under 0.8% across years of processing, well inside the Visa 0.9% and Mastercard 1.5% thresholds.

High-Risk Processing Rates and Rolling Reserves

Most high-risk processors are vague about rates for a reason. They price on what they think they can get away with. We would rather you know what is normal in the category before you apply anywhere, including with us.

Industry-standard high-risk processing rates fall in a range of roughly 2.5% to 5% per transaction, depending on vertical, volume, and prior processing history. CBD topicals and clean-label supplement brands with 3+ months of clean processing data sit at the lower end of that range. New merchants without processing history, higher-sensitivity categories, or prior terminations sit higher. Rates outside this range — either far higher or suspiciously lower — almost always come with a catch in the contract.

A rolling reserve is a percentage of your sales that the acquiring bank holds in reserve to cover potential chargebacks, refunds, and fraud. Across the high-risk category, reserves typically run 5% to 15% of monthly volume, held for 90 to 180 days on a rolling basis. The reserve is yours — it releases back to you on schedule as long as your account stays clean. Rolling reserves are not punitive. They are how the bank makes approving a high-risk category work for both sides.

Your specific rate and reserve depend on your vertical, your volume, your processing history, and your compliance posture. We will quote you honest numbers before you apply and tell you if your business is not approvable in its current form. “Lowest rates in the industry” is marketing language. Real numbers for your specific business is the conversation worth having.

Reserves typically reduce over time as your account performs. A new CBD brand might start at 10% held 180 days and drop to 5% held 90 days after six to twelve months of clean processing. The specific reduction schedule is set with the bank during underwriting and is part of the terms you sign, not a vague promise.

How the High-Risk Merchant Account Application Works

High-risk accounts go through real underwriting. The process takes longer than opening a Stripe account, which is exactly the point — the difference is what creates long-term stability.

1

We review your site for language, labeling, and structural issues that will cause a decline before anything goes to a bank. In high-risk categories this is the single most preventable failure point. We flag what needs to change — FDA disclaimers, “for research use only” language on peptide sites, subscription disclosure, descriptor mismatches — so the application goes in clean the first time.

2

We tell you within 48 to 72 hours whether your business is approvable, at what rate range, and with what reserve structure. No application fee. If your setup is not approvable in its current form, we explain what needs to change — and we do not waste your time applying to a bank that will decline you.

3

Business registration and EIN, government-issued ID for all owners with 25%+ stake, 3 months of business bank statements, 3 months of processing statements if applicable, a voided business check, product labels for active SKUs, and a Certificate of Analysis for CBD or hemp products. Accounts over $100K monthly volume also require two years of tax returns or audited financials.

4

A human underwriter at the acquiring bank reviews your business — products, processing history, bank statements, and website compliance. This is what produces account stability. The bank knows what you sell and has agreed to support it before your first transaction. No surprise review six months in.

5

We configure your Authorize.Net or NMI gateway, set the billing descriptor to match your brand, connect it to your ecommerce platform, and run test transactions. Most merchants with documents in order are fully live within 5 to 7 business days of approval.

6

InclusivePay monitors chargeback alerts, stays available as your volume grows, and is reachable before you make changes that could affect your account — new product categories, marketing campaigns with expected volume spikes, descriptor changes. We stay involved after approval. We do not disappear once you are live.

High-Risk Merchant Account Application Checklist

Have these ready before you apply. A missing document is the most common cause of delays in high-risk underwriting.

Business registration and EIN

LLC, corporation, or partnership documents plus federal EIN letter

Government-issued ID

For all owners with 25% or greater stake

3 months of business bank statements

Business account only — personal statements are not a substitute

3 months of processing history

Required for high-risk categories. Prior statements from Stripe, Square, or any prior processor — even from terminated accounts

2 years of tax returns or audited financials

Required if monthly processing volume exceeds $100K

Voided business check

For deposit account setup

Product labels for active SKUs

Must comply with FDA labeling rules for your category. CBD products need current Certificates of Analysis.

Live, compliant website

FDA disclaimer on supplement product pages, "for research use only" language on peptide sites, return and cancellation policy, privacy policy, terms of service — all visible and current

Prior termination disclosure

If a previous processor shut you down, be upfront. Prior terminations do not automatically disqualify you — hiding them does

What Causes High-Risk Accounts to Fail After Approval

Getting approved is step one. Keeping the account stable is where most high-risk merchants run into trouble — usually for reasons that are avoidable once you know what banks actually monitor.

Visa flags merchants above 0.9% and Mastercard above 1.5%. In high-risk categories this is not a guideline to flirt with — it is an existential line. One bad month with sloppy billing descriptors or a confusing subscription flow can push you into mandatory monitoring, fines, and potential account termination. The most common drivers are billing descriptor confusion, subscription charges customers do not recognize, and efficacy disputes on supplement or CBD products. Our top CBD client runs under 0.8% across 5+ years. The target is hittable — with the right gateway setup, the right descriptor, ClearSale chargeback management, and an accessible cancellation path.

Processors and acquiring banks conduct ongoing website monitoring. A new blog post, a rewritten product description, or an ad campaign that introduces disease treatment language or pharmaceutical comparisons after your account is live can trigger a mid-account compliance review. The standards that got you approved need to stay in place.

A CBD brand that adds a peptide SKU. A supplement brand that launches a weight-loss line. These changes can shift your risk classification mid-account. Run new product additions by us before they go live so we can adjust the underwriting or open a separate account if needed.

A successful influencer post, a podcast mention, or a promotional campaign that triples your monthly volume in a week looks like account fraud to automated risk monitoring. If you are planning a campaign with expected growth, give us a heads up before it runs so we can communicate with the bank in advance.

The harder it is to cancel, the more customers dispute the charge instead of canceling. Every dispute costs you the transaction plus a chargeback fee and edges you toward the monitoring threshold. A visible self-serve cancel button is active chargeback prevention, not just good customer service.

Your Partner in High-Risk Growth

Have these ready before you apply. A missing document is the most common cause of delays in high-risk underwriting.

We know the space

Since 2018, placing high-risk and alternative-health brands with domestic merchant accounts. 500+ brands across CBD, hemp, nutra, peptides, and adjacent verticals.

We underwrite real brands, not short-term cash grabs

We only place businesses that will stay stable with their bank long term. Brands that look like they will blow up the account in six months do not get placed with us. That discipline is why our brands stay live.

We talk to banks and networks daily

Not guesswork. Not stale playbooks. We are in active conversations with acquiring banks about underwriting policy and with networks about evolving category rules — like the 2026 Mastercard BRAM update on research peptides.

We help you grow, not just get approved

Approval is step one. Scaling your volume, adding new product categories, managing chargebacks, swapping gateways without taking your store offline — all of that needs active account management, not a ticketing queue.

You get answers, fast

No black hole of forms. No "we'll escalate to underwriting." 48–72 hour pre-approval with real answers about your specific situation. Reachable by phone, not just email.

Real Clients, Real Volume, Real Stability

Every high-risk processor promises stability. Here is what it actually looks like across three InclusivePay clients — all placed since 2019, all still processing on the same accounts today.

High-volume CBD brand placed in 2019. Over five years of uninterrupted domestic processing with zero account freezes and chargebacks well inside Visa and Mastercard thresholds. This is the upper end of what a properly underwritten CBD account can scale to.

Topical CBD and skincare brand processing through us since 2019. Over $6M in total volume. Chargeback rate under 0.8%. Zero freezes across the entire tenure. The textbook case for what a stable high-risk account should look like.

Research peptide brand placed with a domestic account five-plus years ago. Same account, no issues, no terminations across the entire time peptide compliance enforcement has tightened industry-wide. Proof that research-only ecommerce can stay stable with the right underwriting.

Ready to Stop Playing Payments Whack-a-Mole?

If you are running a serious high-risk business, a properly underwritten merchant account matters more than duct tape and luck. Let’s get your stack dialed in.

- No application fee

- U.S. domestic banks only

- 48–72 hour pre-approval

- Prior terminations accepted

Common questions

High-Risk Merchant Account FAQs

What is a high-risk merchant account?

Can you get CBD merchants approved in the U.S.?

Yes. We specialize in compliant, domestic CBD accounts — topicals, skincare, tinctures, gummies, pet products, hemp flower. Our largest CBD client processes over $2M per month with us. Another topical CBD brand has processed over $6M across 5+ years at under 0.8% chargebacks with zero freezes. For CBD-specific requirements, approval timelines, and supported product types, see our CBD payment processing page.

How long does approval take?

Pre-approval in 48 to 72 hours. Full setup — bank approval, gateway configuration, and first live transaction — typically 5 to 7 business days from submission when your documents are in order. Restricted categories like peptides and cannabis take longer because underwriting is more involved. The most common cause of delays is a missing or incomplete document, not the bank’s speed. We tell you what is missing before anything goes in.

What are your processing rates?

Industry-standard high-risk rates fall between 2.5% and 5% per transaction, depending on vertical, volume, and processing history. Clean-label CBD topicals and established supplement brands with 3+ months of clean processing typically sit at the lower end. New merchants, higher-sensitivity categories, or prior terminations sit higher. Rolling reserves are typical — 5% to 15% held for 90 to 180 days, reducible over time. We quote honest numbers for your specific business during the pre-approval call. “Lowest rates in the industry” is marketing; real numbers for your specific setup is the conversation worth having.

Do you require a rolling reserve?

Yes — rolling reserves are standard across high-risk processing, not specific to InclusivePay. Typical reserves are 5% to 15% of monthly volume, held 90 to 180 days on a rolling basis. The reserve is yours — it releases back to you on schedule as long as the account stays clean. Reserves typically reduce over time as your account performs. A new merchant might start at 10% held 180 days and drop to 5% held 90 days after six to twelve months. The specific schedule is set during underwriting and is part of the terms you sign.

What if I was previously shut down by Stripe, PayPal, or Square?

A prior aggregator shutdown does not disqualify you. Underwriters know the pattern and see it constantly in high-risk categories. The important thing is to disclose it honestly when you apply — trying to hide a prior termination is far more damaging than being upfront about it. We have placed many brands who came to us after a Stripe, Square, PayPal, or Shopify Payments freeze. If you are currently frozen and need to get back online, we specialize in exactly that situation.

What happens if I'm on the MATCH list?

The MATCH list (Member Alert To Control High-risk merchants) is an industry-wide database of terminated merchants. Being MATCH-listed makes approvals harder for up to five years, but it is not a permanent block in every case. Options depend on the reason you were listed — some codes are workable, others require waiting for the five-year timeout. Contact us to discuss your specific situation before applying anywhere. MATCH-listed applicants need a specific underwriting approach, and applying blindly can make the situation worse.

Can I keep my existing payment gateway?

Usually, yes. InclusivePay integrates with Authorize.Net and NMI — the two dominant gateways for high-risk processing. Both connect to Shopify (via compatible plugins), WooCommerce, BigCommerce, ClickFunnels, and custom cart systems. If you are already on Authorize.Net or NMI, we can often route you through the same gateway with a new underlying merchant account. If you are on Shopify Payments or WooPayments, those platforms do not support high-risk, and you will need to migrate to a compatible gateway.

Do you offer recurring billing and subscriptions?

Yes — subscriptions and recurring billing are fully supported when structured correctly. The essentials: clear recurring charge disclosure at checkout, a billing descriptor that matches your store name, an easy self-serve cancellation path, and no free-trial-to-subscription conversions. Free trials that automatically convert to paid subscriptions are prohibited by Visa and Mastercard across every processor — not a preference, a hard network rule. If your current model uses free-to-paid conversion, we help you restructure to what is allowed.

What's the chargeback threshold before I get flagged?

Visa flags merchants above 0.9% and enters mandatory dispute monitoring. Mastercard’s threshold is 1.5%. Both carry monthly fines and potential program termination if you stay above. In high-risk niches, chargebacks are existential — one bad month can end an account. We recommend targeting 0.8% as a buffer and below 0.6% as a real stability zone. We partner with ClearSale for chargeback management and fraud prevention. That plus a clear billing descriptor, 3DS, AVS, and a self-serve cancel path are the core moves for staying well below thresholds.

Can I process internationally?

Yes. We offer both domestic and international processing options. Most U.S.-based high-risk brands are best served by a domestic account with the option to process international cards through the same gateway. Offshore-only processing is available for specific use cases but is not our default recommendation — domestic acquiring is more stable for most operators. We discuss which structure fits during the pre-approval call.

Is InclusivePay a payment processor?

No — InclusivePay is a U.S.-based ISO (Independent Sales Organization) registered with the major card networks. We work directly with domestic acquiring banks to place your business in a properly underwritten merchant account. You know exactly which bank holds your account and processes your transactions. We manage the relationship and stay involved to keep the account stable. This is structurally different from an aggregator like Stripe, which pools thousands of merchants under one master account and monitors them with automated algorithms that do not distinguish between compliant and non-compliant businesses.

Can you help if I'm currently frozen by Stripe or Square?

Yes, and it is a common situation we solve. The frozen funds at your prior processor are not ours to release — those stay on their release schedule (typically 90 to 180 days). What we can do immediately is get you back online with a stable domestic account so you can keep processing new orders while the old freeze releases. Most merchants in this situation are processing on a new account within 5 to 7 business days of reaching out.

What makes InclusivePay different from other high-risk processors?

Three things. First, we are domestic — U.S.-based ISO, U.S. acquiring banks, no offshore routing or opaque pooling. Second, we specialize across CBD, nutra, peptides, and adjacent verticals rather than claiming to do everything — each category has different underwriting and we know each one. Third, we stay involved after go-live. Active account management, chargeback monitoring, heads-up calls before campaigns, and a real human to reach when something changes. Most of our clients came to us after a bad experience with a processor that disappeared after onboarding. We do not.