Written by the InclusivePay Merchant Advisory Team | Last updated: April 2026

InclusivePay has been placing CBD merchants since 2018. This guide covers what underwriters actually look for — not just the document checklist.

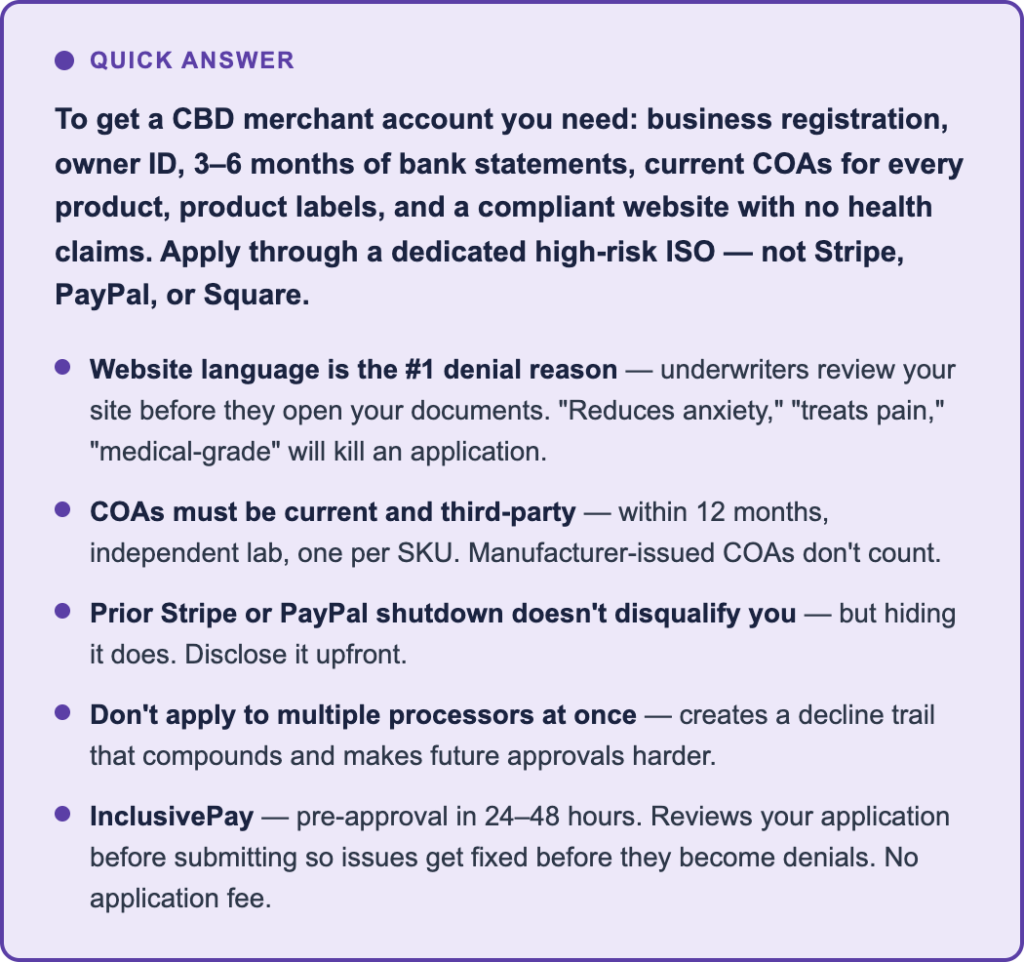

Let’s skip the preamble. You want to know what it actually takes to get a CBD merchant account approved and keep it open. Not the generic document checklist — the real stuff underwriters care about that nobody tells you before you apply.

The merchants who get denied aren’t usually missing documents. They’re getting flagged on their website, or they’ve got outdated COAs, or they’re applying through the wrong channel. Sometimes all three. Here’s how to not be that merchant.

What Underwriters Actually Look At First

Here’s something that surprises most merchants: underwriters typically review your website before they open your application documents. Your site is the fastest signal of whether you’re a compliant, stable business or a termination risk waiting to happen.

They’re looking for health claims. Any language that could be interpreted as a disease treatment claim — even subtle phrases — is an instant red flag. Not just on product pages. FAQs, blog posts, meta descriptions, customer review widgets, testimonials. All of it gets scanned.

They also check your return policy, your COA accessibility, your checkout flow, and whether your product descriptions match what you said you sell. A messy, inconsistent site raises questions about how carefully you run your business. A clean, compliant site signals the opposite.

| Real consequence: We’ve seen complete, well-documented applications declined because of a single blog post with a health claim. Clean your entire site — not just product pages — before you apply. |

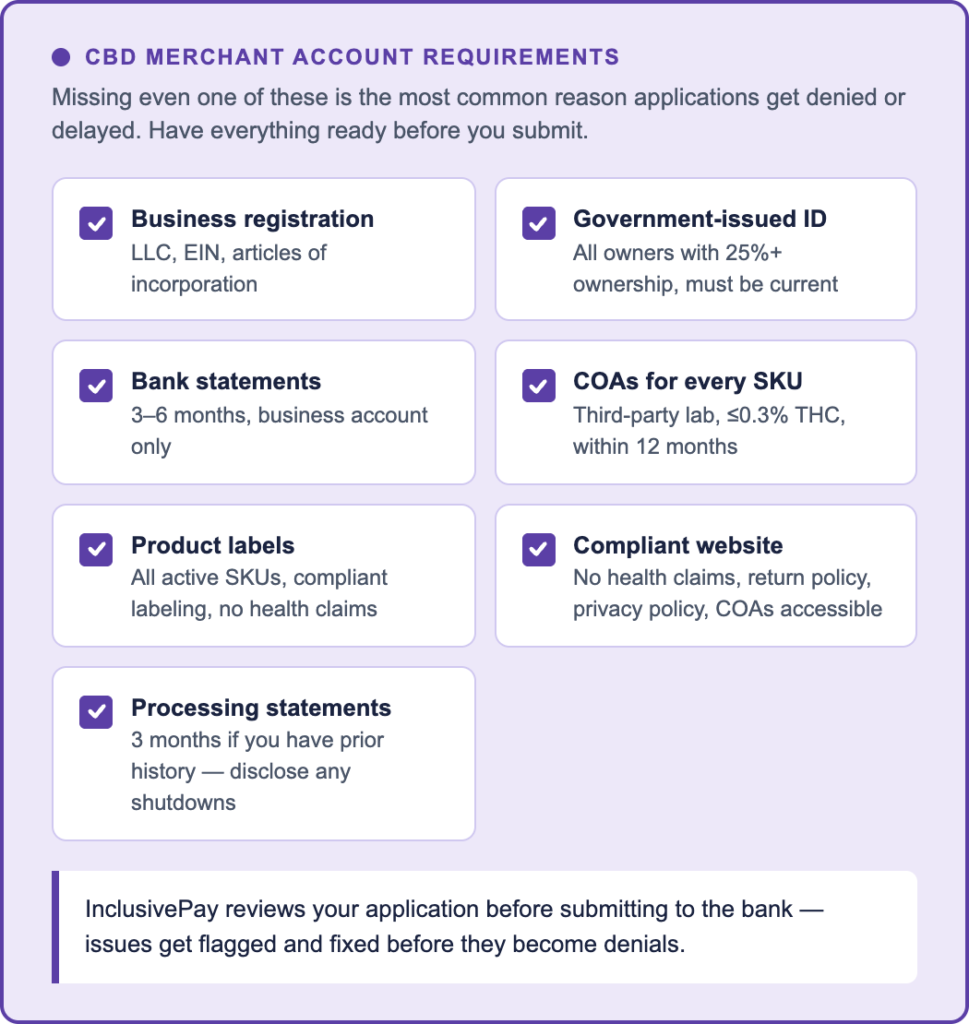

The Complete Requirements Checklist

Here’s everything you need, and what each item actually needs to look like to pass underwriting:

- Business registration: LLC operating agreement or articles of incorporation, EIN confirmation letter. Must show the legal entity that will hold the merchant account.

- Government-issued ID: For every owner with 25% or more ownership. Driver’s license or passport. Must be current — expired ID causes delays.

- Business bank statements: 3–6 months minimum. Must show consistent business activity. Red flags: very new account with no history, large unexplained deposits, overdrafts. Statements should be from the account where merchant funds will settle.

- Certificates of Analysis (COAs): Third-party lab only — not your manufacturer’s own testing. Delta-9 THC at or below 0.3%. Within the last 12 months. One COA per product SKU. The COA must show the full cannabinoid profile, not just THC. Missing a COA for even one SKU can delay the whole application.

- Product labels: All active SKUs. Must be compliant — no health claims, ingredient list, serving size, batch number, manufacturer information. Labels that look like they make drug claims will slow things down.

- Live compliant website: Product descriptions with no health claims, clear return/refund policy, privacy policy, terms of service, accessible COAs (either linked on product pages or available on request). Checkout flow should be clean and functional.

- Processing history (if applicable): 3 months of statements from any prior processor. Chargeback ratio visible. Prior history is a positive signal — even if you’ve had shutdowns. Disclose them upfront.

The Mistakes That Kill Applications

Based on what we see across hundreds of CBD merchant account applications, here are the most common reasons merchants get denied or delayed:

- Health claims on the website: The #1 reason. “Reduces anxiety,” “treats pain,” “helps with sleep,” “anti-inflammatory,” “medical-grade” — any of this kills the application or, worse, gets you approved and then flagged six months later during ongoing monitoring.

- Outdated COAs: COAs older than 12 months are treated as expired. Some banks require them to be even more current — within 6 months for ingestibles. If you have seasonal products, keep COAs current year-round.

- Manufacturer-issued COAs: A COA from your supplier’s own lab doesn’t count. It needs to be third-party — an independent lab with no financial relationship to your manufacturer.

- Applying to multiple processors at once: Every application creates a record. Multiple applications in a short window look like you’ve been declined elsewhere. Apply to one specialist at a time, starting with the best fit for your product category.

- Hiding a prior termination: Underwriters run checks. A prior Stripe or PayPal shutdown will show up. If you disclose it proactively, it’s a normal situation with a known explanation. If they find it themselves, it looks like you were trying to hide something.

- Volume mismatch: Understating your volume to seem lower-risk, then exceeding it quickly after approval, triggers an automated review. Be accurate about your actual and projected volume from the start.

- Missing SKUs: Applying for a merchant account covering 10 products and only providing COAs for 3 is a mismatch. Every product you’ll be processing must be documented.

How the Approval Process Actually Works

Here’s what happens from the moment you apply to the moment you’re live:

- Application review: InclusivePay reviews your application and documentation. We flag any issues before submitting to the acquiring bank — so you get a chance to fix problems rather than just receiving a denial.

- Pre-approval: For most CBD merchants, this comes within 24–48 hours. Pre-approval means the acquiring bank has reviewed your business and is willing to proceed. It’s not the same as full approval — the gateway isn’t live yet.

- Underwriting: The bank’s underwriting team does a full review of your documents, website, product catalog, and processing history. This is where COA issues and website language problems surface. For standard CBD (topicals), this typically takes 3–5 business days. For ingestibles (oils, edibles), allow 7–10 days.

- Gateway setup: Once underwriting is complete, your payment gateway (Authorize.Net or NMI) is configured and tested. InclusivePay handles this setup.

- Go live: Test transactions are run to confirm everything processes correctly. You’re given the gateway credentials and integration instructions for your ecommerce platform.

The whole process for a standard topical CBD account with complete documentation is typically 5–7 business days. For CBD oil and ingestibles, 7–10 days. The biggest variable is how quickly documentation issues get resolved — which is why having everything ready before you apply matters.

After Approval: Keeping Your Account Open

Getting approved is step one. These are the things that keep a CBD merchant account open long-term:

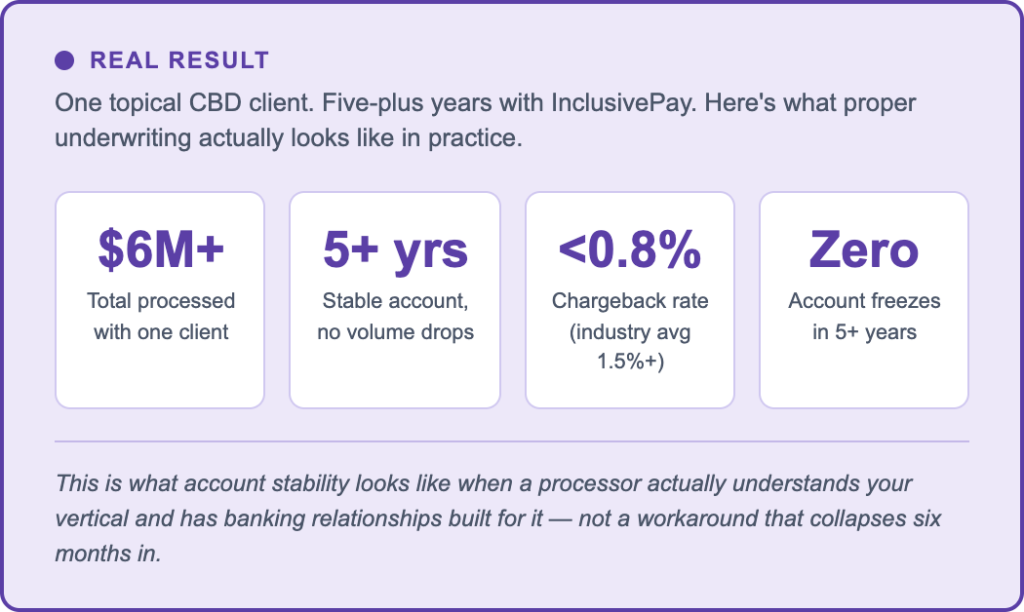

- Keep chargebacks below 1% Visa and Mastercard both have chargeback monitoring programs that flag merchants above 1%. Aim for 0.8% or below. For CBD oil and ingestibles, a clear product description and transparent return policy eliminates most disputes before they start.

- Maintain site compliance after approval Processors do ongoing website monitoring. A new blog post with health claims, an updated product description with treatment language, or a new testimonial that implies medical benefit can trigger a mid-account review.

- Keep COAs current Set a calendar reminder. An expired COA during ongoing monitoring is a compliance flag even if your original application had everything current.

- Notify your processor before volume spikes A sudden 3x volume increase looks like fraud to automated risk systems. If you’re running a sale or scaling ad spend, give InclusivePay a heads-up.

- Don’t add new product categories without checking Adding ingestibles to a topicals-only account, or delta-8 to a CBD-only account, changes your risk profile mid-account. Check with us before adding new product types.

FAQs

What do I need to get a CBD merchant account?

Business registration (LLC, EIN), government-issued ID for all owners with 25%+ ownership, 3–6 months of business bank statements, current COAs for every product (third-party lab, ≤0.3% Delta-9 THC, within 12 months), product labels, and a compliant website with no health claims. Processing statements from any prior processor if you have them. For ingestibles, some banks also require supplier/manufacturer agreements.

How long does CBD merchant account approval take?

With InclusivePay, pre-approval for most CBD merchants comes within 24–48 hours. Full setup with your gateway live is typically 5–7 business days for topicals and 7–10 business days for oils and ingestibles. The biggest variable is how quickly documentation issues get resolved — complete documentation upfront is the single biggest factor in approval speed.

Why do CBD merchant account applications get denied?

The most common reasons: health claims on the website (the #1 reason), outdated or manufacturer-issued COAs, missing COAs for some SKUs, prior processing history with elevated chargebacks, or applying to the wrong type of processor. Most denials are fixable — they’re about gaps in documentation or compliance, not fundamental eligibility issues.

Can I get a CBD merchant account if Stripe or PayPal already shut me down?

Yes. Aggregator terminations for CBD are very common and don’t disqualify you. The important thing is to disclose the prior shutdown upfront. See our guide to what to do after a Stripe or PayPal shutdown for the full step-by-step.

What is a COA and why do I need one for every product?

A Certificate of Analysis is a test report from a third-party lab confirming the cannabinoid content of your product — specifically that Delta-9 THC is at or below 0.3%. It must be from an independent lab (not your manufacturer’s own testing), current within 12 months, and covering every product SKU you sell. Missing a COA for even one product delays the entire application.

Do I need processing history to get approved?

No. New businesses without processing history get approved for CBD merchant accounts regularly. Processing history is a positive signal — it shows your business is established and lets underwriters see your chargeback ratio — but it’s not required. Without processing history, the weight shifts more heavily to your website compliance, COAs, and business documentation.

What’s the difference between a CBD merchant account and a payment gateway?

A merchant account is the bank relationship that allows you to accept card payments. A payment gateway (Authorize.Net, NMI) is the software layer connecting your store to that account. For CBD you need both. See our WooCommerce and Shopify CBD gateway guide for platform-specific integration details.

Does InclusivePay help with the application process?

Yes. InclusivePay reviews your application before submitting to the acquiring bank — issues get flagged and fixed before they become denials. See our CBD payment processing page for full details. No application fee.

The Bottom Line

Getting a CBD merchant account approved isn’t complicated — it’s just specific. The merchants who get denied are almost always dealing with fixable issues: website language, outdated COAs, or applying to the wrong type of processor.

Get the setup right before you apply. Clean site, current COAs for every SKU, complete documents, dedicated high-risk ISO. That’s the whole formula. It works consistently.

InclusivePay has been placing CBD merchants since 2018. If you want us to review your application before you submit it, reach out here — no application fee, no pressure, just a straight answer on whether everything looks good.

– InclusivePay Merchant Advisory Team | inclusivepay.com | Updated April 2026