Written by the InclusivePay Merchant Advisory Team | Last updated: April 2026

InclusivePay has been placing CBD merchants since 2018. This guide reflects what we’ve seen work — and what merchants consistently get wrong about CBD credit card processing rates and setup.

Here’s a question we hear constantly: “Why is CBD credit card processing so expensive?” Sometimes it is. But often the merchant is just on the wrong type of plan — a legacy flat-rate setup from 2019 when options were scarce — and hasn’t realized the market has changed significantly since then.

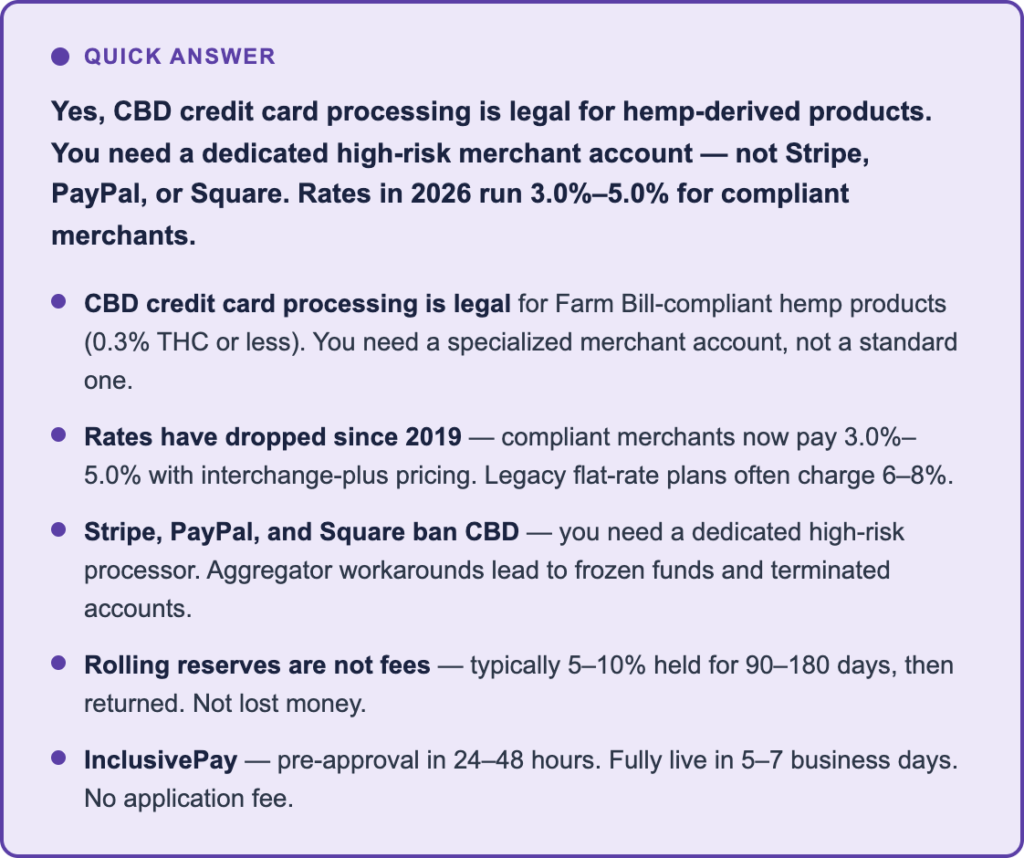

CBD credit card processing in 2026 is more accessible, more competitive, and cheaper than it’s ever been. Stripe, PayPal, and Square still ban it, but the dedicated high-risk processor market has matured. If you’re compliant and you come with your paperwork in order, you shouldn’t be paying more than 5%. If you are, it’s time to look at your options.

This guide covers how CBD credit card processing actually works, what rates you should expect in 2026, what the fees mean, and how to get set up properly.

Is CBD Credit Card Processing Legal?

Yes — with conditions. The 2018 Farm Bill federally legalized hemp-derived CBD products containing 0.3% THC or less. That means hemp CBD businesses can legally accept credit and debit card payments. The catch is that the banking and card network infrastructure hasn’t fully caught up with legalization, so most mainstream processors still treat CBD as high-risk or prohibit it outright.

What does that mean practically? Stripe, PayPal, and Square explicitly ban CBD in their terms of service. Visa and Mastercard permit CBD processing — but only through acquiring banks that have specifically approved the merchant category. That’s why you need a dedicated high-risk merchant account, not a standard one.

The legal complexity varies by state. Some states have additional regulations on top of federal law — labeling requirements, age restrictions, sales restrictions on certain product types. Your processor and your website need to reflect whatever state-level rules apply to where you sell. A good CBD processor will flag compliance issues before they become account issues.

How CBD Credit Card Processing Actually Works

Understanding the flow helps you understand why rates are what they are. Here’s what happens every time a customer pays with a card on your CBD store:

- Customer checks out: Their card data is captured by your payment gateway (Authorize.Net, NMI) and encrypted.

- Gateway routes to your merchant account: The gateway sends the transaction to the acquiring bank holding your merchant account.

- Acquiring bank requests authorization: The bank contacts Visa or Mastercard, who contact the customer’s card-issuing bank.

- Authorization is approved or declined: The issuing bank approves based on available funds and fraud signals. Response comes back in seconds.

- Funds are captured and settled: Approved funds are held, fees are deducted, and the net amount settles to your merchant account — typically within 1–3 business days.

- Ongoing compliance monitoring: Your processor monitors transaction patterns, chargeback ratios, and your website for compliance. This is ongoing, not just at approval.

The reason CBD accounts cost more than standard retail is steps 2 and 3 — the acquiring bank that’s willing to hold CBD transactions is taking on more regulatory and chargeback risk than a standard bank would. They price for that. The more established your business and the cleaner your compliance, the better rates you can negotiate.

What Does CBD Credit Card Processing Actually Cost in 2026?

This is where most guides get vague. Let’s be specific.

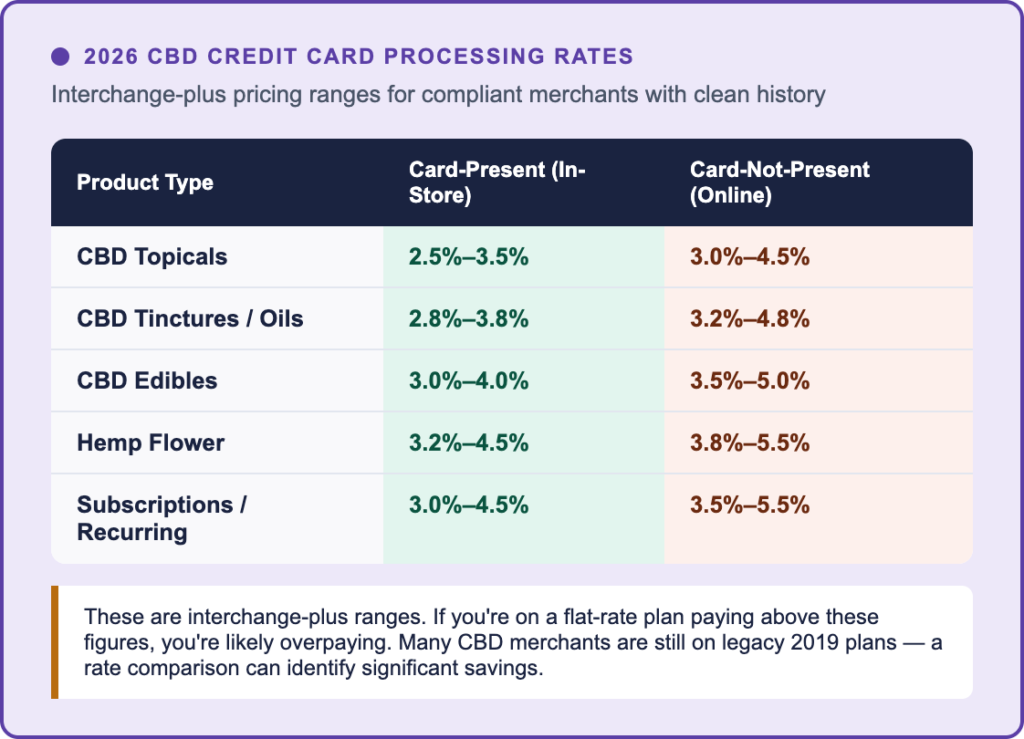

The market has changed dramatically since the early days after the 2018 Farm Bill when merchants had few options and paid 7–8% just to process at all. In 2026, compliant CBD merchants with clean history can get interchange-plus pricing in these ranges:

| Product Type | Card-Present (In-Store) | Card-Not-Present (Online) |

| CBD Topicals | 2.5%–3.5% | 3.0%–4.5% |

| CBD Tinctures / Oils | 2.8%–3.8% | 3.2%–4.8% |

| CBD Edibles | 3.0%–4.0% | 3.5%–5.0% |

| Hemp Flower | 3.2%–4.5% | 3.8%–5.5% |

| Subscriptions / Recurring | 3.0%–4.5% | 3.5%–5.5% |

| Note: These are interchange-plus ranges. If you are on a flat-rate plan paying above these figures, you are likely overpaying. Many CBD merchants are still on legacy 2019 flat-rate plans — a rate comparison can identify significant savings. |

The debit card opportunity: Here’s something worth knowing: with interchange-plus pricing, regulated debit cards process at their actual interchange rate, which can be as low as 0.05% + $0.21. On a flat-rate plan you pay the same 5%+ regardless of card type. For CBD businesses with significant debit card volume, switching to interchange-plus can reduce fees on those transactions by 40–60%.

The Fees You’ll Actually Encounter

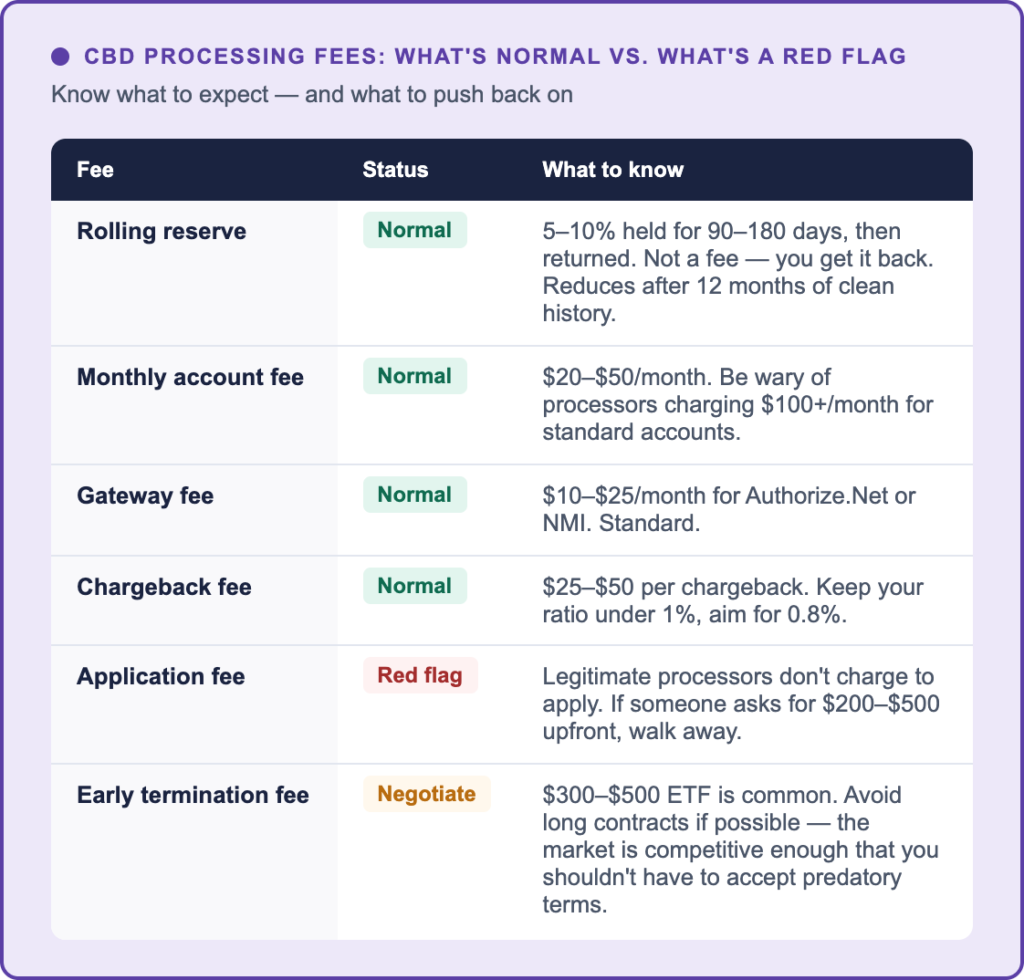

Beyond the per-transaction rate, here are the fees that show up on CBD merchant accounts — and what’s normal vs. what’s a red flag.

| Fee | Status | What to know |

| Rolling reserve | Normal | 5–10% of monthly volume held for 90–180 days, then returned. This is NOT a fee — it’s a temporary hold the acquiring bank uses as a cushion against chargebacks. You get it back. New accounts and higher-risk product types (edibles, flower) typically see larger reserves. After 12 months of clean history, most merchants can negotiate the reserve down or eliminate it. |

| Monthly account fee | Normal | $20–$50/month for account maintenance, statements, and compliance monitoring. Reasonable. Be wary of processors charging $100+/month for standard accounts. |

| Gateway fee | Normal | $10–$25/month for Authorize.Net or NMI. Standard. |

| Chargeback fee | Normal | $25–$50 per chargeback. Standard across high-risk processing. The real cost of chargebacks is the ratio — too many and your account gets flagged. Keep it under 1%, aim for 0.8%. |

| Application fee | Red flag | Legitimate processors don’t charge application fees. InclusivePay charges none. If someone’s asking for $200–$500 upfront just to apply, walk away. |

| Early termination fee | Negotiate | Some processors lock you in with ETFs of $300–$500. Avoid long contracts if you can, or negotiate this out. The market is competitive enough that you shouldn’t need to accept predatory contract terms. |

The Billing Descriptor Problem Nobody Talks About

Here’s something most CBD processing guides completely skip: your billing descriptor is one of the biggest drivers of chargebacks, and most merchants don’t pay attention to it until it’s too late.

A billing descriptor is what appears on your customer’s credit card statement. If your descriptor is something generic like “HLTH PRODUCTS LLC” or your processor’s name rather than your brand name, customers don’t recognize the charge. They call their bank and dispute it. That’s a chargeback — and it happens before they even try to contact you.

Fix: Work with your processor to set a clear, recognizable descriptor — ideally your brand name or store name. Something your customer will recognize when they see it on a statement three weeks after purchase. This one change can reduce “friendly fraud” chargebacks by a meaningful amount. It’s especially important for subscription CBD businesses where customers may forget a recurring charge.

Card-Not-Present vs. Card-Present — Why Online CBD Sellers Pay More

If you’re selling CBD online, you’re processing card-not-present (CNP) transactions. This means the physical card isn’t swiped or tapped — the customer types in their number. Banks charge more for CNP transactions because fraud and chargebacks are statistically higher when the card isn’t physically present.

This is why online CBD stores typically pay 0.5%–1.0% more per transaction than retail CBD stores. It’s not CBD-specific — all online merchants pay more than in-person merchants for this reason. CBD just compounds it because the category already carries a higher base rate.

If you run both in-store and online: If you run both in-store and online sales, your processor should be able to give you different rate tiers for each. Don’t accept a blended rate that prices your in-person transactions at your online rate — you’re leaving money on the table.

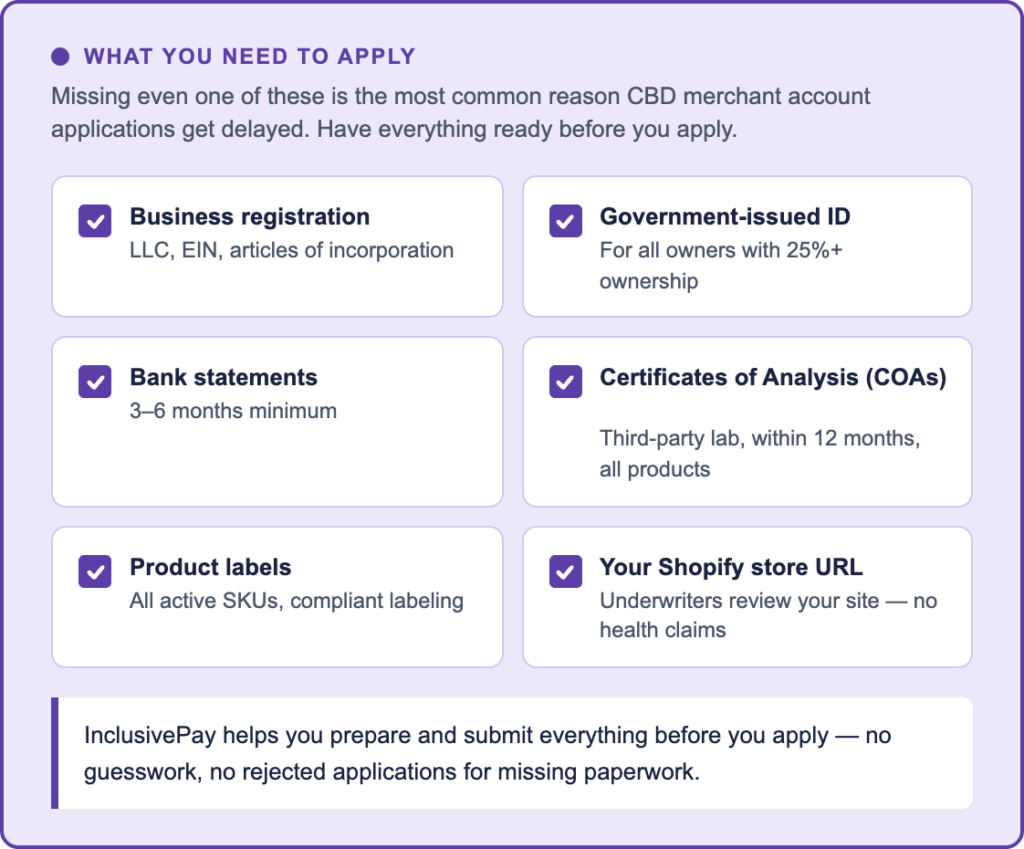

What You Need to Get Approved

Getting approved for CBD credit card processing isn’t complicated if you come prepared. Here’s what every processor will need:

- Business registration documents — LLC, EIN, articles of incorporation

- Government-issued ID for all owners with 25%+ ownership

- 3–6 months of business bank statements

- Certificate of Analysis (COA) for every product — third-party lab, Delta-9 THC at or below 0.3%, within 12 months

- Product labels for all active SKUs

- Live, compliant website — no health claims, clear return policy

- Processing history if you have it — 3 months of statements from any prior processor

Your website matters more than most merchants expect. Underwriters review your product pages, your claims, and your checkout flow before approving the account. Language like “treats anxiety,” “cures pain,” or “medical-grade” will get your application denied or your approved account flagged later. Clean it up before you apply.

Approval timeline: With InclusivePay: pre-approval in 24–48 hours for most CBD merchants. Fully live in 5–7 business days for standard CBD. Hemp flower and edibles may take slightly longer depending on the acquiring bank.

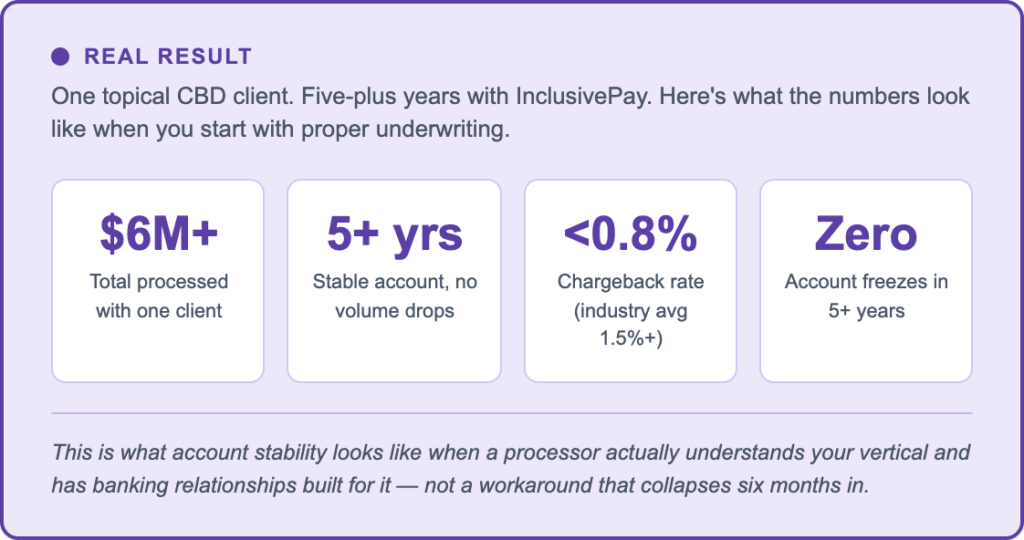

| REAL RESULT One topical CBD brand has processed over $6M with InclusivePay across 5+ years. No volume drops. Chargebacks held under 0.8%. Never frozen. That’s what a properly underwritten account looks like long-term. |

FAQs

What payment processors allow CBD?

Dedicated high-risk processors including InclusivePay, PaymentCloud, Easy Pay Direct, Bankful, and Durango Merchant Services all support CBD. Stripe, PayPal, and Square’s standard platform explicitly prohibit it. See our full comparison of CBD payment processors for a detailed breakdown of each option.

What are typical CBD credit card processing rates in 2026?

With interchange-plus pricing through a specialized processor, compliant CBD merchants typically pay 3.0%–4.5% for card-present (in-store) transactions and 3.5%–5.5% for card-not-present (online) transactions. Product type matters — topicals run lower than edibles or hemp flower. If you’re paying above these ranges on a flat-rate plan, you’re likely overpaying and should get a rate comparison.

Is CBD credit card processing legal?

Yes, for hemp-derived CBD with 0.3% THC or less, CBD credit card processing is federally legal under the 2018 Farm Bill. The complication is that most mainstream banks and processors still treat CBD as high-risk, which means you need a dedicated merchant account rather than a standard one. See our high-risk merchant account guide for the full explanation.

What is a rolling reserve in CBD payment processing?

A rolling reserve is a percentage of your monthly processing volume — typically 5–10% — that the acquiring bank holds for 90–180 days as a buffer against chargebacks. It is not a fee and you do get it back. After 12 months of clean processing history, most merchants can negotiate the reserve down significantly or eliminate it. New accounts and higher-risk product types (edibles, flower) typically have larger initial reserves.

How do I get a CBD merchant account?

Apply through a dedicated high-risk ISO like InclusivePay. You’ll need business registration documents, ID for all owners, 3–6 months of bank statements, current COAs for all products, product labels, and a compliant website. InclusivePay pre-approves most CBD merchants in 24–48 hours. See our CBD payment processing page for the full application process.

What is a CBD billing descriptor and why does it matter?

Your billing descriptor is what appears on your customer’s credit card statement. If customers don’t recognize the charge, they dispute it — that’s a chargeback even if the purchase was legitimate. Set your descriptor to your brand name or store name. This is especially important for subscription CBD businesses. Work with your processor to configure this before you go live.

Can I use Shopify or WooCommerce for CBD credit card processing?

Yes — but not with the default payment options. Shopify Payments runs on Stripe and bans CBD. For both platforms, you need a third-party gateway (Authorize.Net or NMI) connected to a dedicated CBD merchant account. See our WooCommerce CBD gateway guide and Shopify CBD payment processing guide for platform-specific setup details.

What happens if Stripe or PayPal freezes my CBD account?

Stop processing on any other aggregator immediately. Gather your transaction logs and termination notice. Then apply for a dedicated high-risk merchant account. A prior Stripe or PayPal shutdown doesn’t disqualify you. See our guide to what to do when Stripe or PayPal shuts you down for the full step-by-step.

The Bottom Line

CBD credit card processing isn’t as hard or as expensive as it used to be. The market has matured, rates have dropped, and compliant merchants with clean documentation can get approved quickly and pay reasonable fees.

The merchants who struggle are almost always in one of two situations: they used an aggregator that eventually shut them down, or they got onto a flat-rate legacy plan in 2019 and never reviewed their rates. If you’re in either of those situations, it’s worth having a conversation about what a properly structured account actually looks like.

InclusivePay has been placing CBD merchants since 2018. If you want a straight answer on rates and whether we can help, reach out here — no application fee, no pressure.

– InclusivePay Merchant Advisory Team | inclusivepay.com | Updated April 2026