Written by the InclusivePay Merchant Advisory Team | Last updated: April 2026

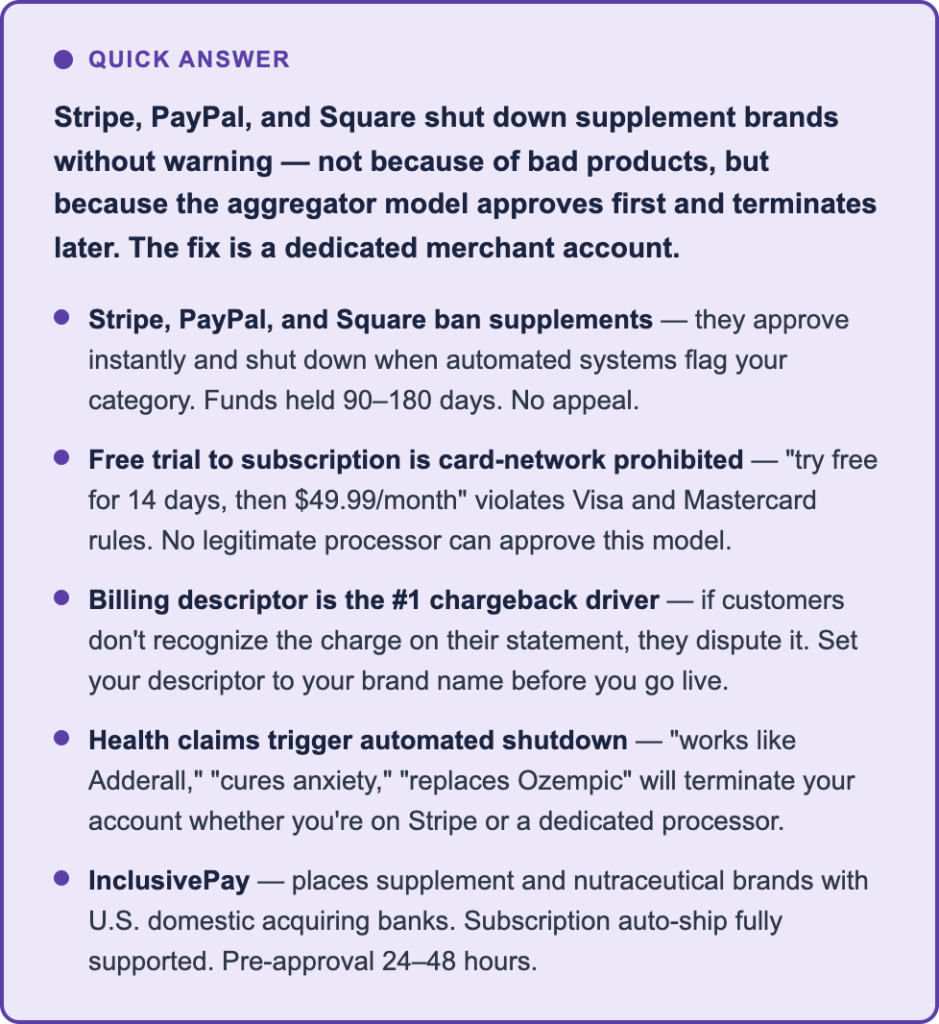

InclusivePay has been placing supplement and nutraceutical merchants with U.S. domestic acquiring banks since 2018. This guide covers what actually happens when aggregators shut down supplement businesses — and the setup that keeps accounts stable long-term.

If you’re reading this, there’s a decent chance something already went wrong. Maybe Stripe just froze your account. Maybe PayPal is holding $30,000 in pending payouts with no explanation. Or maybe you’re building a supplement brand and doing the research before it happens.

Here’s what most payment processing guides won’t tell you upfront: being shut down as a supplement brand has nothing to do with whether your products are legitimate. You can have clean ingredients, a compliant website, proper FDA disclaimers, and a spotless chargeback history — and still wake up to a termination email. We’ve seen it happen to nootropics brands doing $22K a month with zero prior disputes. Square flagged “cognitive enhancer” in their product descriptions. $14,000 in pending payouts was held for 93 days.

The processor isn’t the problem. Using the wrong type of processor is.

Why Stripe, PayPal, and Square Keep Failing Supplement Brands

Stripe, PayPal, and Square are payment aggregators. They don’t underwrite your business before approving you. They pull everyone into a shared merchant pool, approve instantly with automated systems, and let their risk algorithms sort things out later. When those algorithms flag your products — and they will, because supplements consistently trigger the same patterns as other restricted categories — your account gets frozen without a human ever reviewing your business.

The categories that trigger it most reliably: weight loss supplements, nootropics and cognitive enhancers, immune support with any disease language, pre-workout with stimulant profiles, and anything marketed with health outcome claims. It doesn’t matter if your claims are compliant. The category itself is enough.

| Real consequence: Stripe and PayPal hold funds for 90–180 days after termination. You cannot withdraw, cannot process new sales, and may be placed on the MATCH list — a database of terminated merchants that makes future approvals significantly harder for up to five years. Fully compliant brands get shut down constantly. |

The other thing worth knowing: Shopify Payments runs on Stripe infrastructure. If you’re using Shopify Payments for your supplement store, you have the same problem with a different logo on it. You need a third-party gateway regardless of which ecommerce platform you’re on.

The Free Trial Problem Nobody Explains Clearly Enough

This one catches supplement brands constantly. Free trial offers that automatically convert to a paid recurring subscription are prohibited by Visa and Mastercard card network rules. Not Stripe’s preference. Not a risk management choice. A hard card network rule.

Real consequence: The specific model that’s prohibited: “try free for 14 days, then $49.99/month unless you cancel.” This model cannot be approved by any legitimate processor — dedicated or aggregator — because the card networks won’t allow it. If your current model works this way, no ISO can approve it either. Contact us before applying to discuss how to restructure.

Standard subscription programs — where the customer explicitly agrees to a recurring charge at the time of purchase — are fully supported and work well for supplement brands. The difference between a subscription model that stays stable and one that generates chargebacks usually comes down to four things: a recognizable billing descriptor, a disclosed recurring charge at checkout, a self-serve cancellation path, and pre-billing email reminders. We’ll cover these below.

The Subscription Billing Descriptor Problem

Here’s something most payment processing guides completely skip: your billing descriptor is one of the biggest drivers of chargebacks for supplement brands, and most merchants don’t pay attention to it until it’s too late.

Your billing descriptor is what appears on your customer’s credit card statement. If it says “HLTHSTACK LLC” instead of your brand name, customers don’t recognize the charge. They call their bank and dispute it. That’s a chargeback — and it registers as a dispute before anyone ever contacts you. For supplement brands running subscription auto-ship, this is the single biggest source of “friendly fraud” chargebacks.

The fix: Work with your processor to set a clear, recognizable descriptor — your brand name or store name, recognizable to a customer three weeks after purchase. This is especially critical for supplement subscription businesses. One change, dramatic reduction in disputes.

What to Do Right Now If Your Account Was Frozen

- Don’t apply to another aggregator: The instinct after a Stripe shutdown is to immediately sign up for a Square or PayPal account. Don’t. A second aggregator shutdown compounds your MATCH list risk. Stop the aggregator cycle entirely.

- Document everything: Transaction logs, the termination notice, bank statements, product documentation, your business registration. You need all of this for your next application.

- Check your MATCH list status: Not every aggregator termination triggers a MATCH listing, but supplement shutdowns with elevated chargebacks can. Contact InclusivePay — we can help assess your status before you apply anywhere.

- Audit your website language: Before applying anywhere, remove every health claim that implies treatment, cure, or prevention of a disease. Remove any comparison to prescription drugs. Check every page — product listings, blog posts, FAQs, meta descriptions.

- Apply through a dedicated specialist: A dedicated high-risk ISO underwrites your business before approval. The acquiring bank knows what you sell before your first transaction. That prior agreement is what makes the account stable in a way aggregator accounts never are.

Product Claims That Will Get Your Application Declined

In the supplement space, what your website says is as important as what your products contain. These phrases are automatic application killers — and cause mid-account shutdowns even for approved accounts:

- Any claim that implies treatment, cure, or prevention of a disease — cancer, diabetes, Alzheimer’s, depression, ADHD, anxiety disorders

- Comparisons to prescription drugs — “works like Adderall,” “replaces Ozempic,” “as effective as antidepressants”

- “FDA approved,” “clinically proven,” or any framing that implies regulatory clearance you don’t have

- Guaranteed results or extreme before/after claims — “lose 30 pounds in 30 days guaranteed”

- Missing FDA disclaimer on individual product pages — it must appear on each product page, not just the site footer

Language like “supports healthy cognitive function,” “promotes relaxation,” and “helps maintain energy levels” is generally acceptable. The line is between structure-function claims (acceptable) and disease claims (not). If you’re unsure, run your copy by InclusivePay before applying — we see what gets accounts declined every day.

Aggregators vs. InclusivePay for Supplement Processing

| Feature | Stripe / PayPal / Square | InclusivePay |

| Supplements allowed? | Volatile — commonly shut down | Yes, properly underwritten |

| Underwriting | None — auto-approved instantly | Full, before first transaction |

| Account stability | Frozen without warning | Stable, ongoing support |

| Funds held on termination | 90–180 days | Not applicable |

| Subscription auto-ship | High shutdown risk | Fully supported when structured correctly |

| Free trial to subscription | Prohibited by card networks | Also prohibited — we explain alternatives |

| Chargeback support | None | Monitoring and prevention tools |

| U.S. domestic bank | Aggregator pooled account | Direct domestic bank placement |

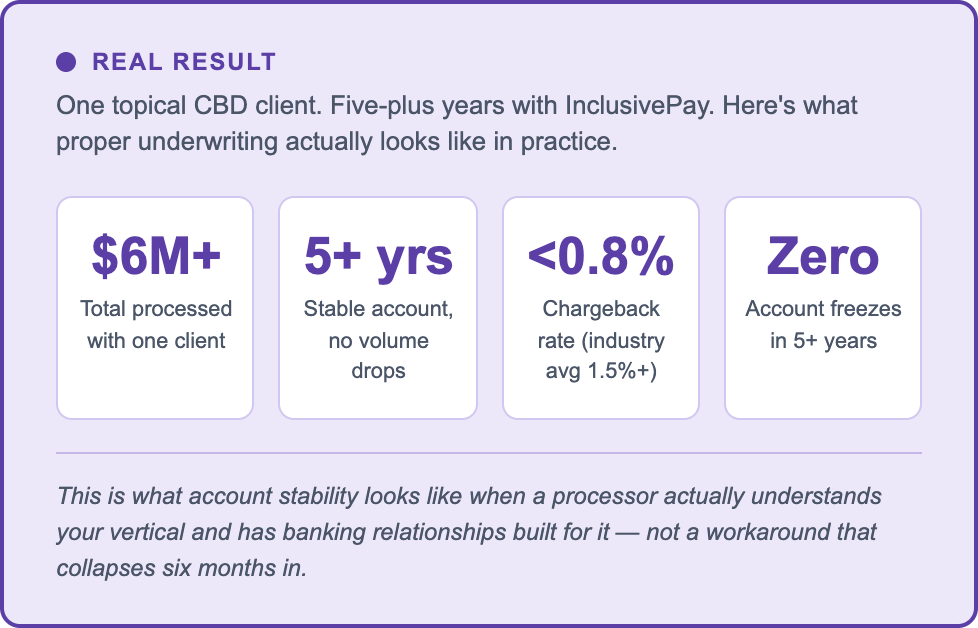

| REAL RESULT One topical CBD brand has processed over $6M with InclusivePay across 5+ years. No volume drops. Chargebacks held under 0.8%. Never frozen. We bring the same underwriting discipline to supplement and nutraceutical accounts. |

FAQs

Does Stripe allow supplement sales?

Not reliably. Stripe approves supplement merchants instantly but shuts them down when automated risk systems flag the category. See our guide on what to do when Stripe shuts you down for the step-by-step after a shutdown.

Does PayPal allow supplement sales?

PayPal has the same aggregator model as Stripe — instant approval, delayed risk enforcement. Supplement brands with health claims, elevated chargeback patterns, or subscription billing models are flagged regularly. PayPal has a documented pattern of holding supplement merchant funds for 180 days after termination. It’s not a reliable long-term option for serious supplement brands.

Can I use Shopify Payments for my supplement store?

Not if you want stability. Shopify Payments runs on Stripe. Disable it and connect a third-party gateway. See our nutraceutical merchant account page for supplement-specific setup details.

Are free trial supplement offers allowed?

Free trial offers that automatically convert to a paid subscription are prohibited by Visa and Mastercard card network rules — not just by individual processors. “Try free for 14 days, then $49.99/month unless you cancel” cannot be approved by any legitimate processor. Standard subscription programs where the customer explicitly agrees to a recurring charge at checkout are fully supported. Contact us before applying to discuss how to restructure a free trial model.

What supplement categories are hardest to get approved?

Weight loss and fat burners carry the highest chargeback risk due to efficacy disputes. Nootropics and cognitive enhancers face the most claims scrutiny. Anything with prescription drug comparisons is an automatic decline. Vitamins, minerals, and basic supplements are the easiest to approve. See our nutraceutical merchant account page for a full breakdown by supplement subcategory.

Can I get a supplement merchant account if Stripe or PayPal already shut me down?

Yes. Aggregator terminations for supplement brands are extremely common and don’t automatically disqualify you. Disclose the prior shutdown upfront — underwriters find out anyway, and hiding it is far more damaging than disclosing it. If you were MATCH-listed, the situation is more complex but not hopeless. Contact us to discuss your specific history.

What does a supplement merchant account cost?

Rates depend on your specific product category, volume, and chargeback history. Standard supplements (vitamins, minerals) run lower than weight loss or nootropic categories. Most accounts start with a rolling reserve of 5–10% of monthly volume held for 90–180 days — this is returned, not lost. InclusivePay does not charge application fees. Rates are disclosed before you sign anything.

Does InclusivePay work with subscription supplement brands?

Yes. Subscription auto-ship is the dominant model in the supplement space and InclusivePay fully supports it when structured correctly — explicit recurring charge disclosure at checkout, recognizable billing descriptor, self-serve cancellation, and pre-billing reminders. Free trial to subscription models cannot be approved (card network rule). See our nutraceutical merchant account page for full details on subscription billing requirements.

The Bottom Line

Most supplement brands don’t fail because of a bad product or a compliance issue. They fail because their payment processing collapses at the worst possible moment — during a launch, a subscription scale, or right after they’ve invested in ads.

The processors that work for this category do one thing differently: they underwrite your business before you start processing, not after. That single difference — underwriting upfront versus automated approval with delayed termination — is what separates a stable payment setup from a ticking clock.

InclusivePay has been placing supplement and nutraceutical brands since 2018. If you want a straight answer on whether we can help with your specific product catalog and business model, reach out here — no application fee, no pressure.

– InclusivePay Merchant Advisory Team | inclusivepay.com | Updated April 2026